In startup funding, there are hubs where most investments originate and there are so-called venture deserts, where deals hardly ever happen. And then there are places in the middle, which see a steady, but not massive, number of funding rounds.

Usually when we talk about startup hubs we’re referring to metro areas. But the categorization can apply to countries as well. For as long as we’ve been tracking, a handful of nations rake in the vast majority of startup venture funding while others get virtually none.

Subscribe to the Crunchbase Daily

Here, we’re going to look at the middle ground–a group of roughly 10 countries that bring in between $1 billion and $3 billion a year in early- and late-stage venture funding.* For want of a catchier term, we’ll call them moderate-sized markets.

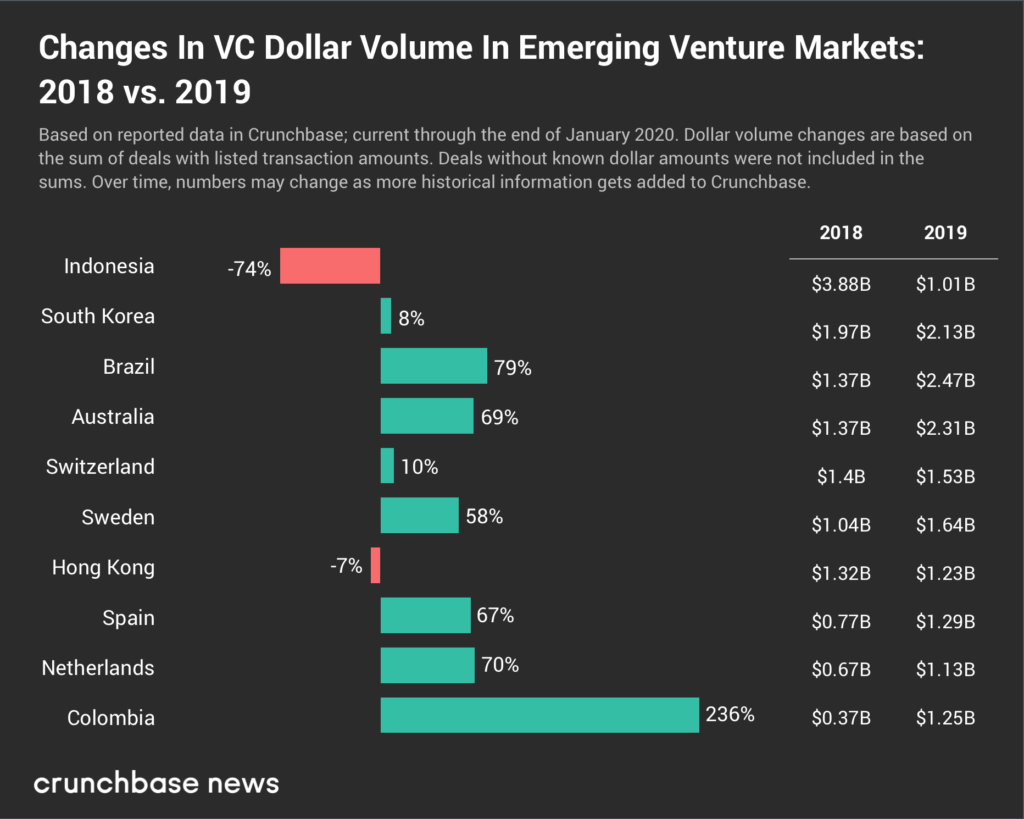

It’s a geographically diverse bunch. Three hail from Asia: Indonesia, South Korea and Hong Kong. Two are in Latin America: Brazil and Colombia. Four are from Europe: Spain, Sweden, Netherlands and Switzerland. And then there’s the lone continent, Australia

Putting it in perspective

You may be wondering how these mid-sized venture regions compare to the really big hubs. As it turns out, even when taken altogether, they’re rather tiny in comparison.

To put it in perspective, U.S. startups raised over $100 billion in reported financing rounds in 2019. The group of 11 countries we’re featuring here collectively brought in less than one-eighth that amount.

But while they may be small compared to the big hubs, moderate-sized markets are far more dynamic. To get a better idea of how the countries in this grouping rank, we’ve charted out funding for each in the past two years:

Totals for the moderate-sized markets fluctuate a lot more than the larger ones. If we saw a 236 percent annual increase in U.S. venture funding, or a 74 percent decline, investors would be freaking out. In the moderate-sized markets, it’s quite common to see increases or declines of 50 percent or more.

Here are some other findings:

Giant deals skew totals: Seeing big fluctuations in national funding totals year over year doesn’t necessarily signal a more bullish or bearish overall investment climate. That’s largely because really big rounds for one or more companies can really skew the results.

Take Indonesia, for example. In 2018, local ride-hailing wunderkind Gojek pulled in over $2.4 billion, which accounted for most of the venture for the entire country. A dip in funding totals for 2019 says less about the national startup investment climate than about Gojek’s fundraising schedule.

In Colombia, meanwhile, e-commerce unicorn Rappi was the main reason funding for the whole country surged in 2019. It closed a $1 billion round backed by SoftBank.

Reported round counts fall below 150 a year: For this dataset, we looked at how many disclosed venture rounds of Series A or later closed in each country over the course of 2019.

While no one is on track to rival the United States’ thousands of rounds per year, the numbers are pretty encouraging in that they point to a solid foundation of funded companies already making it past seed stage.

Most funding increases are due to bigger rounds, not more deals: More than half the countries on our list reported year-over-year funding increases of over 50 percent. Yet when looking at round counts, most countries, based on data to date, were flat to down.

Rounds frequently get reported late, and that may lead to upward revisions. However, the basic trendline is pretty clear: Investments rose more than deal counts. That means backers are putting more money into the startups they like, but not necessarily doing a lot more deals at Series A and beyond.

Wrapping up

So, what area is poised to become the next big venture hub? We’ll study that question in more detail next week, as we hone in on the fastest-growing startup funding markets.

For now, it’s safe to surmise that countries bringing in a few billion a year in startup funding today have plenty of more room to grow.

* We focused on early and late stage (Series A and beyond) and did not include seed-stage funding rounds. This is due in part to the pattern of seed-stage rounds being reported in Crunchbase weeks or months after they close, which can make results for recent quarters appear lower than warranted. While reporting delays also occur at Series A and beyond, they are less pronounced. Small seed rounds, particularly in non-English-speaking countries, may have a higher likelihood of not being included in the dataset.

Illustration: iStock

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of stopwatch - AI [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/Halftime-AI-1-300x168.jpg)

67.1K Followers