Apparently, venture investment doesn’t always go up.

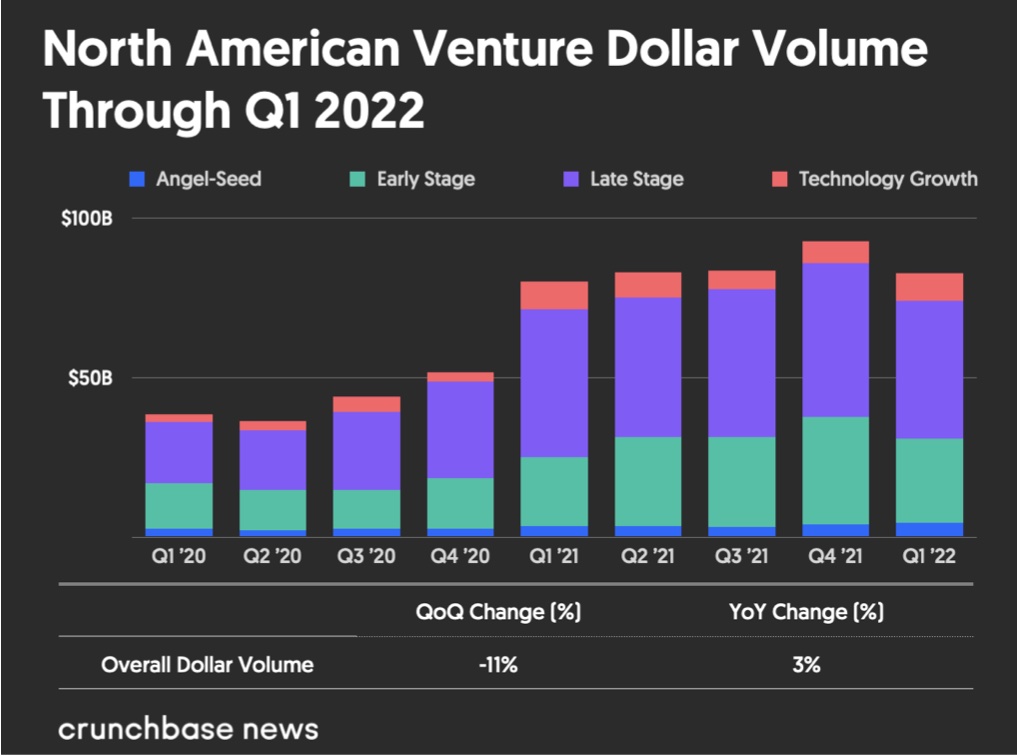

That’s the key finding from our tally of North American startup investment in the first quarter. Altogether, investors put $82.8 billion into seed through growth-stage technology investments in the first quarter of 2022—down 11 percent from Q4 of 2021.

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

It’s the first quarter-over-quarter decline in nearly two years. And while the total is still historically high—the fourth-biggest on record—it does suggest that the red-hot startup investment climate of recent quarters is cooling down some.

You can see that broad trend illustrated in the chart below:

Potential causes for a decline are easy to name. Geopolitical tensions, inflation, rising interest rates and growing investor concerns around ultra-rich unicorn valuations are all affecting the private markets. Then there’s the mostly shuttered IPO window, paired with disappointing aftermarket performance for many recent debuts.

However, it’s also sensible to avoid sounding too negative. While things are down quarter over quarter, Q1 2022 tallies are still up by around 3 percent from the same period last year. Big-ticket deals also continue to close at a brisk pace, with a whopping 156 early- and late-stage rounds of $100 million and up.

Below, we highlight top trends, looking at investment by stage, round counts, largest funding recipients and major exits.

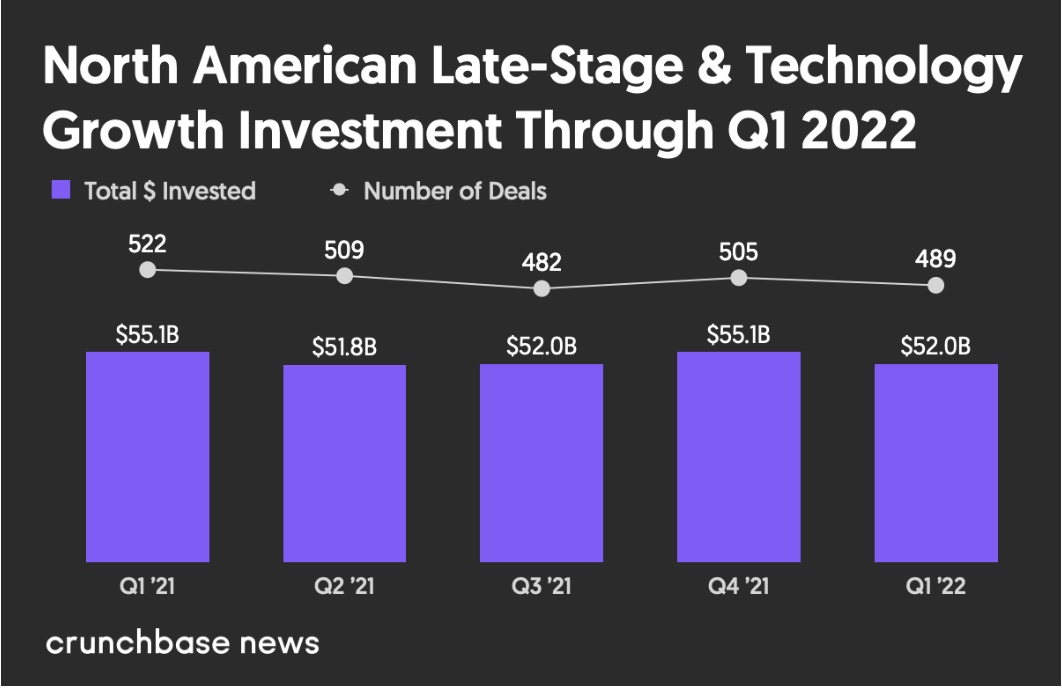

Late-stage and technology growth

We’ll start with late-stage, where most startup investment gets spent.

A total of $52 billion went to North American late-stage and technology growth rounds in Q1 2022. That’s down around 6 percent from both Q4 and Q1 of 2021, which both came in at around $55 billion.

Round counts, meanwhile, totaled 489, down a bit from both the prior quarter and the year-ago quarter. For a broader picture, we lay out investment totals and round counts for the past five quarters in the chart below:

A handful of really large late-stage rounds played a big role in pushing up North America’s totals. The largest late-stage round went to Flexport, a freight forwarding and logistics platform that pulled in $935 million in a February Series E round led by Andreessen Horowitz.

Next up were Cross River, a fintech and financial services provider, and 1Password, a password manager, each of which raised a $620 million round.

While big deals got done, we also learned that lofty valuations set in 2020 and 2021 can go down. Most notably, grocery delivery decacorn Instacart closed out the quarter by disclosing that it will slash its valuation by nearly 40 percent to $24 billion, down from $39 billion.

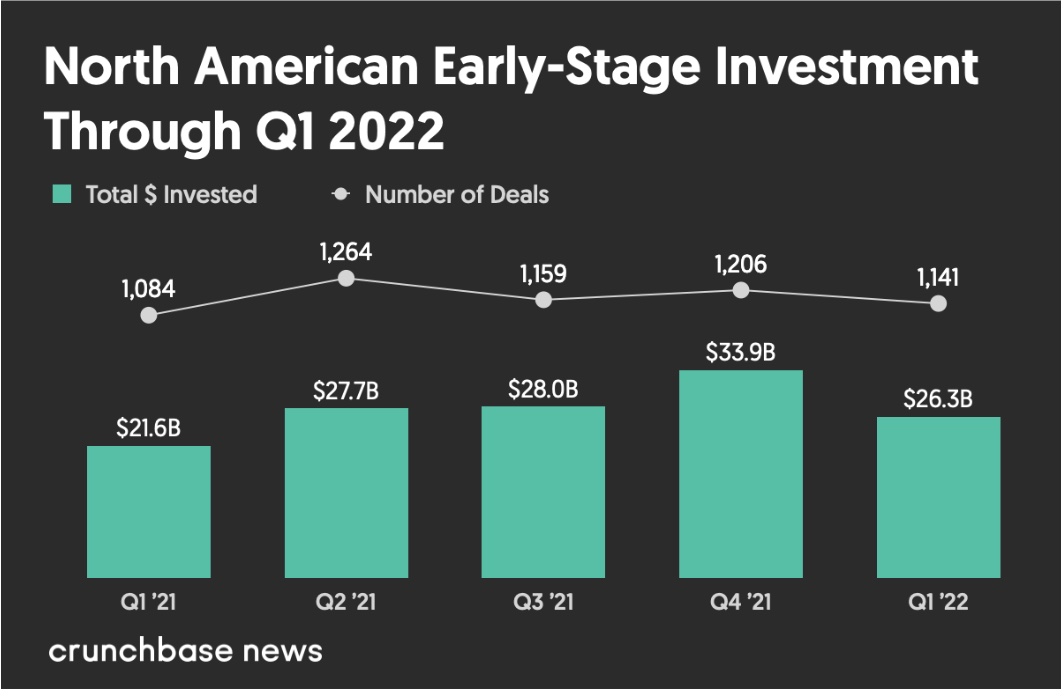

Early stage

After hitting record highs in Q4, early-stage funding (Series A and B), slowed sharply in Q1.

Investors put a total of $26.3 billion into early-stage startups in North America in Q1, down 22 percent from the prior quarter. But while that’s a steep drop, it may mostly be just an indicator of how crazy things got in Q4.

Even with the quarter-over-quarter decline, early-stage investment for Q1 2022 was actually much higher than the year-ago period; roughly median performance for the past five quarters, as laid out in the chart below:

Early-stage round counts—which totaled 1,141—were within the average range for the past five quarters. The general trend seems to be that we’re below the peaks, but the startup funding scene is still running hot.

A few really enormous rounds stood out at the early stage. The biggest was a $518 million Series B for Eikon Therapeutics, a Hayward, California-based developer of technology to analyze single molecule protein behavior in living cells. The next-biggest were crypto trading platform FTX, which landed a $400 million Series A, and shapewear brand Skims, which picked up a $240 million Series B.

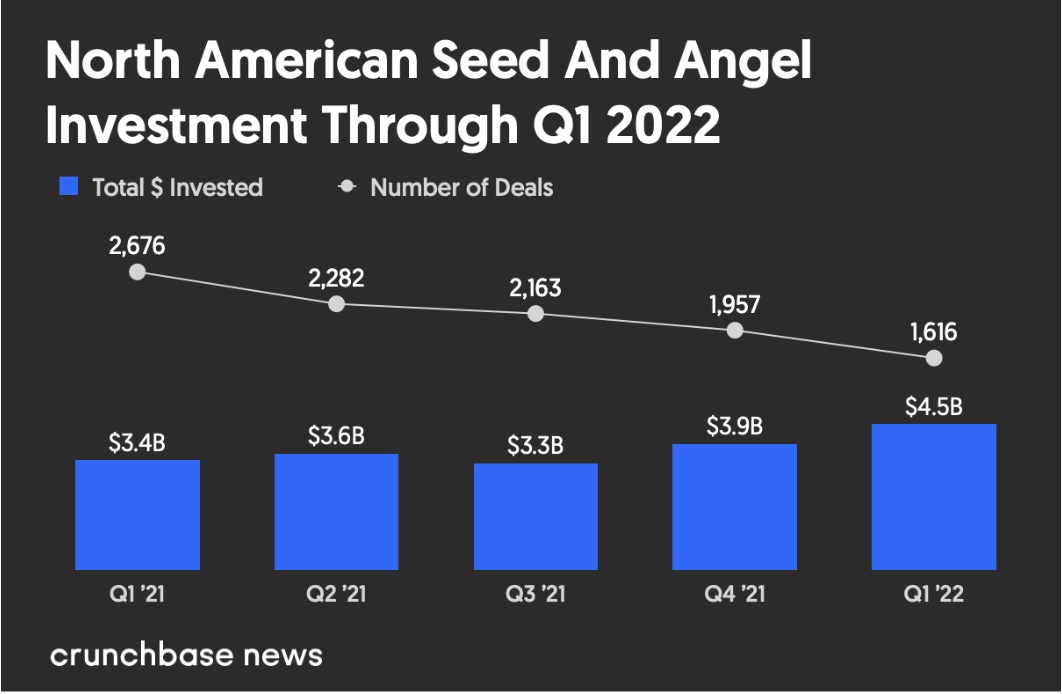

Seed-stage funding

Seed funding hit a record level in Q1 2022, even as other investment stages posted declines.

Altogether, investors put $4.5 billion into reported seed deals in North America in the first quarter, up 14 percent from the prior quarter and a whopping 33 percent higher than the year-ago quarter.

For perspective, we lay out funding and round counts for the past five quarters below:

Much of the reason for the jump stems from the fact that some ultra-large rounds were categorized as seed. This includes a $450 million March round for Yuga Labs, the NFT startup known for its Bored Ape Yacht Club collection.

Over the years, investors have also become increasingly comfortable backing larger rounds at the seed stage. While it used to be rare that such deals exceeded seven figures, times have changed. Now it’s pretty common to see seed rounds of $10 million and up, with 77 logged in the Crunchbase dataset for Q1 alone.

Exits

The first quarter produced mixed results on the exit front. We look at the breakdown below:

IPOs

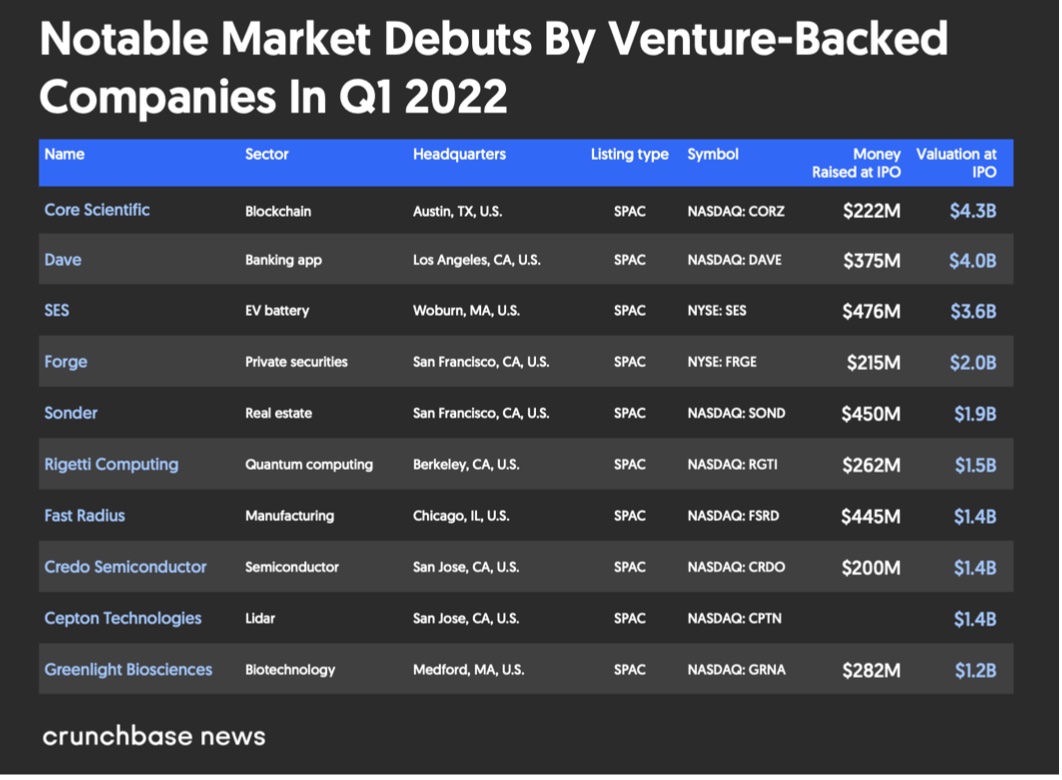

Far fewer venture-backed companies carried out public market debuts in Q1 compared to other recent quarters. However, there were some good-sized debuts, including several previously announced SPAC combinations that completed mergers. We highlight 10 of the largest ones below:

The IPO market was very quiet in terms of new filings for public offerings. Most of the venture-backed companies that went public did so by completing mergers announced last year with blank-check acquirers. In fact, nine of the 10 companies listed above did SPAC deals. The only traditional venture-backed IPO on the list is semiconductor company Credo.

M&A

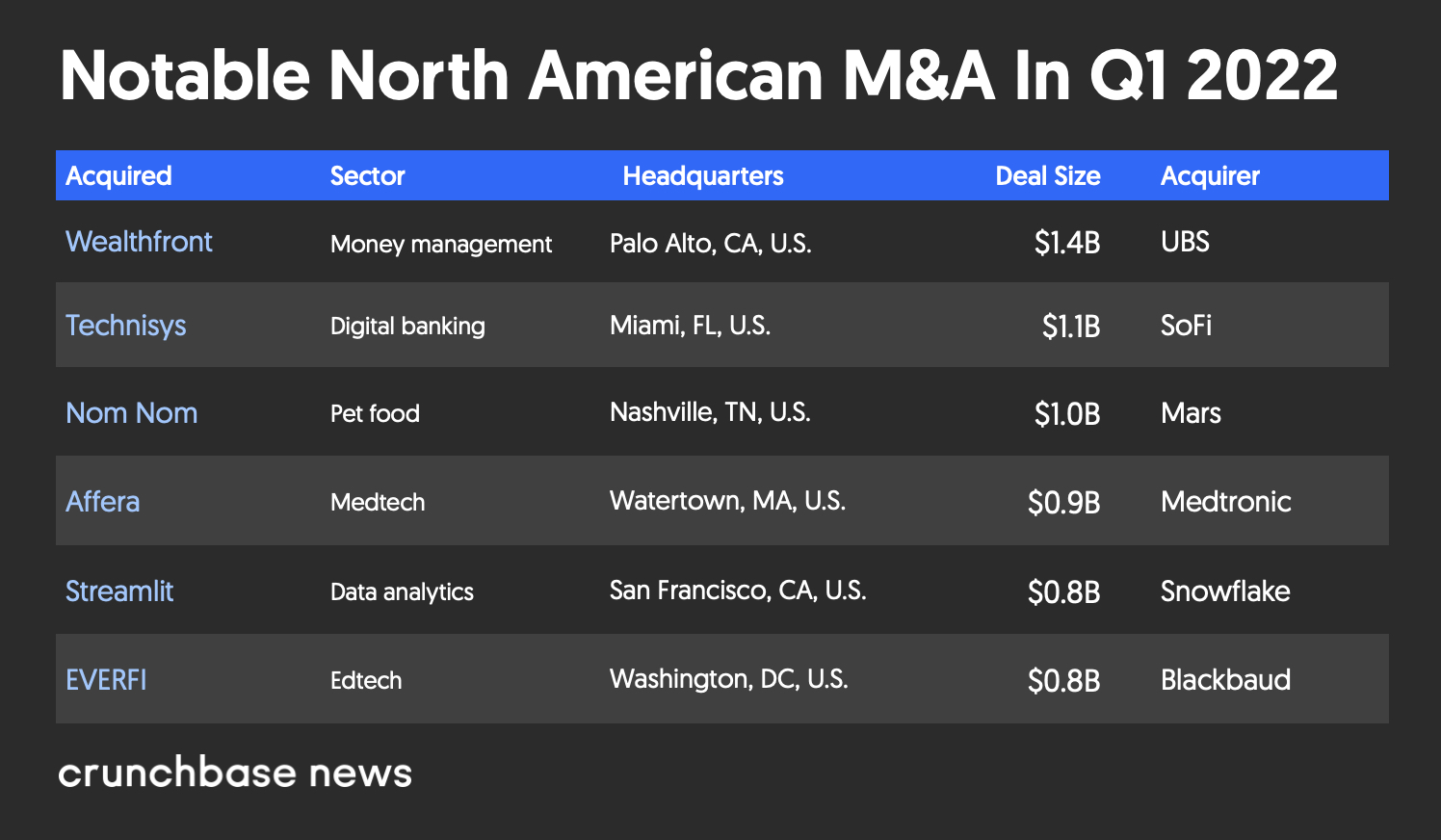

Acquirers continued to snap up venture-backed companies in Q1, including some good-sized deals. We lay out six of the larger ones below:

The largest M&A transaction involving a private, venture-backed company was the sale of wealth management platform Wealthfront to UBS for $1.4 billion. Founded in 2008, Wealthfront previously raised more than $200 million in venture funding.

Next up in deal size is Technisys, a provider of digital banking technologies acquired by SoFi for around $1.1 billion. Miami-based Technisys previously raised around $64 million in known funding.

In summary

Overall, investment in the startup sphere is down from its peaks but still running pretty hot by historical standards. Where are the trends headed?

To look month-by-month at Q1, it seems things are trending lower rather than higher. Total funding across stages in January was just over $31 billion. For February and March it was closer to $25 billion and $26 billion, respectively.

The fact that March’s totals are a bit higher than February’s prevents us from running with the narrative of an obvious continuing slowdown. But clearly, we have crested the peak of the last cycle and now are somewhere on the other side.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of pandemic pet pampering. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/2021/03/Pets-2-300x168.jpg)

67.1K Followers