Congratulations, you have a buyer interested in your company. Negotiations over the purchase price, which is arguably the most critical factor, are the center of this negotiation.

What is earnout?

Earnout is often used to bridge “purchase price gaps” between a buyer and seller. For example, a seller wants $120 million for its business, but the buyer only wants to pay $100 million at closing. However, the buyer is willing to pay an additional $20 million after closing if certain post-closing milestones are met.

Subscribe to the Crunchbase Daily

This deferred payment reduces some of the purchase price risk, especially if the target is an emerging growth company without a lot of operational history and there is some uncertainty about its business model or projections. This could make it a win-win for both buyer and seller if done correctly via an earnout.

When a portion of the purchase price in M&A consists of contingent payments that are payable after closing within a specified period of time, such payments are commonly referred to as an “earnout.” The typical earnout provision entitles the seller to further payments if the target company, post-closing, meets certain agreed benchmarks which can be financial (revenue or earnings targets) or milestone driven (product release, getting regulatory approval or winning a desired customer contract).

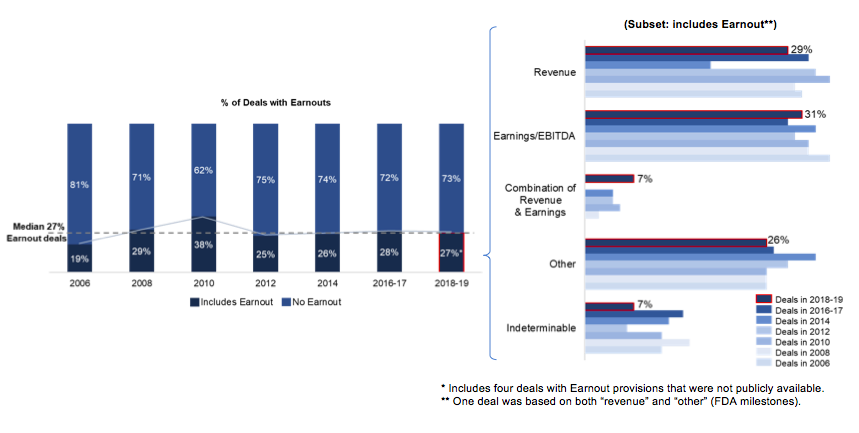

The chart below from the American Bar Association (ABA) shows the use of earnout over the last few years which on average has been used in one out of four deals. The chart on the right shows how the earnout have been paid over different metrics in time from ABA.

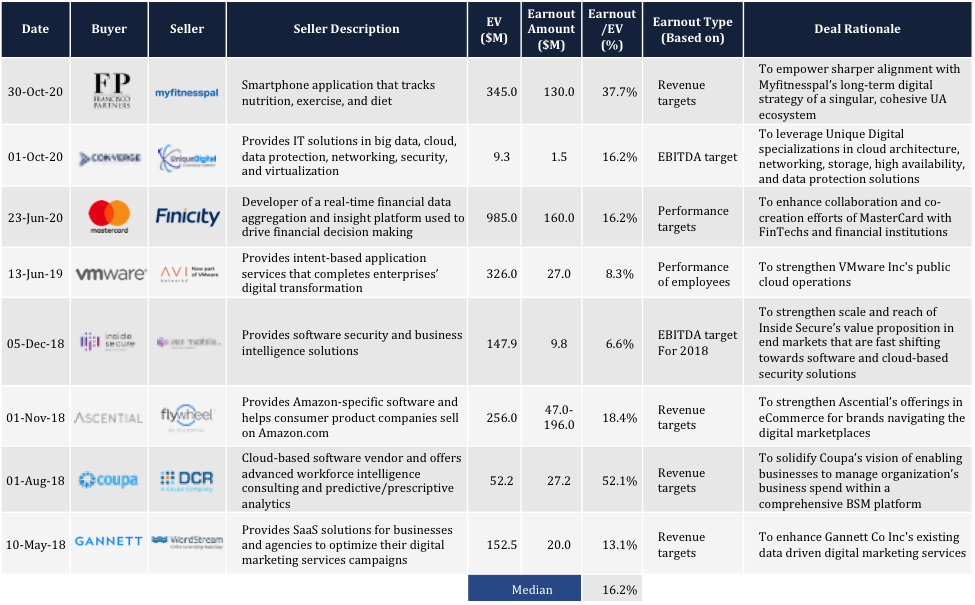

Examples of earnout in selected recent technology transactions:

What to look out for in an earnout plan:

1. Earnout benchmarked to financials (Revenue, EBITDA)

In most M&A deals post-closing, the seller’s business gets integrated into the buyer’s business and from a seller’s perspective it is best to use an earnout target based on revenue targets vs. EBITDA targets.

There are many variables that go into calculating EBITDA and as one moves down the income statement, the costs assigned to the seller’s business by the buyer can cause EBITDA targets to be missed.

Generally, in technology companies, there is more focus on revenue growth vs. EBITDA optimization unless it is a mature technology company or if the seller is being acquired by a private equity firm which is EBITDA focused on valuation.

Revenue-based targets are always easier to measure and help to avoid disputes later on benefiting both parties. Sellers should also ensure that the earnout is on a sliding scale vs. all or nothing.

For example, if the revenue target for end-of-year one post-close is $100 million and the seller’s business achieves $95 million growing from $80 million, the seller should get (15/20=75 percent) of the value of the earnout vs. getting nothing if they hit $95 million. This also benefits the buyer as sellers might give up on increasing revenue and lose motivation if they get the sense that they will not be receiving any payments if the revenue targets are not achievable.

2. Milestone driven

For technology companies, earnout may be paid on the release of a new product, integration of the product with the buyer’s technology etc. Both parties should take care in defining when a milestone is met and how resources will be allocated by the buyer post-close to meet the milestone in a timely manner.

3. Period of the earnout and what happens to earnout on change of control

Generally a shorter period of earnout helps both parties as buyers have a higher administrative burden in managing and tracking the earnout over a longer time frame and sellers have higher uncertainty. Sellers asking for acceleration of earnout on change of control is strongly suggested as a new buyer may not have the same motives for the seller as the original buyer. If the buyer does not agree to acceleration upon change of control, a compromise might be to include a buyout option wherein they can choose to pay the seller and not want the existing earnout to create issues in their impending sale to another party.

4. Covenants to run the business consistent with past practice after closing to achieve earnout

While sellers often ask buyers for legal assurances, buyers do not want to run the business with constraints; hence we rarely see such provisions being included in the purchase agreements. Buyers will make promises to the sellers that they intend to pay the full earnout but will want freedom to operate their business in a manner which serves the buyer. Hence it is important that the purchase price at close be satisfactory to the seller as earnout is a contingent payment.

Summary

We look at earnout as “icing on the cake” and would recommend that sellers pursue a transaction if the upfront purchase price is appealing. Earnout should ideally be no more than 10-20 percent of the total purchase price for a seller’s business that is generating revenue and growing.

Sellers should ensure that in the purchase agreement there is language around how disputes as it relates to earnout will be handled via a third party.

Sellers may also want to consider discussing retention-based payments that are above and beyond normal compensation in exchange for a portion of the earnout as these are typically structured as cash or stock payments if the seller stays employed in a satisfactory manner with the buyer’s business for a certain period of time.

We have observed that levels of earnout have slightly increased due to increased uncertainty created by the COVID-19 pandemic. This impacts valuation and purchase price and increases the use of earnout as a tool to bridge the valuation gap.

This article provides a high-level overview of earnout. For detailed specific cases, it’s best to discuss with your advisors (bankers, lawyers) and feel free to reach out to us.

Gaurav Bhasin is managing director with Allied Advisers, a global technology-focused boutique advisory firm headquartered in Silicon Valley (with presence in Los Angeles, Tel Aviv and Mumbai) focused on investment banking for entrepreneurs and investors.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of a guy watering plants with a blocked hose - Global [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/quarterly-global-3-300x168.jpg)

67.1K Followers