Financial services remained the leading sector for venture investment in 2022 despite an overall pullback in venture funding and shockwaves in the crypto industry. And fintech is expected to remain strong in 2023, with areas from payments to accounting management likely to lead the way.

Payments could remain the most-funded sector within fintech, especially startups focused on B2B payments. On the other side, cryptocurrency and blockchain, which experienced a large increase in funding in recent years, will most likely face a pullback in the wake of FTX’s collapse.

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

Leading sectors

Venture investment into fintech companies in 2022 reached $81 billion as of Dec. 14 — down 41% so far from the peak of 2021 at $137 billion. Still, that $81 billion figure still exceeds 2020 amounts by more than $30 billion.

All told, the sector has grown more than 10 times in the last decade from $7 billion in 2013.

Within the fintech sector, payments- and banking-related startups received the most venture funding over the past five years, Crunchbase data shows. Cryptocurrency startup funding exceeded these two leading sectors in 2021, but dropped back a bit in 2022. Blockchain technology also received more funding in 2021 and grew its share into 2022.

E-commerce and insurance, meanwhile, fell as a proportion of overall dollars invested.

First innings in fintech

The fintech sector is still in early innings, according to a recent report from venture firm Coatue that analyzes the changes modern fintech has brought to the world of finance.

The New York-based firm, an investor in private and public company stocks, wrestles with the question of value creation in the fintech sector in the report on the state of fintech.

Of the $11 trillion in market capitalization in financial services companies as of October 2022, only $508 billion — 2% — was in modern fintech companies, Coatue notes. That proportion was higher in 2021 at 5% due to high valuations given to public technology stocks, but in prior years it did not reach 1%.

“On the way up everybody values growth,” Michael Gilroy, the co-head of its fintech practice and co-COO of Coatue’s growth practice, said in an interview. “On the way down, everybody is valuing profitability and retention. The highest-quality business models within fintech have actually been hit a lot less than the rest of the market.”

There is a large amount of gross profit for modern fintechs to eat into: Across the financial services sector, gross profits globally totaled $6.5 trillion in 2021, Coatue estimates.

Fintech business models

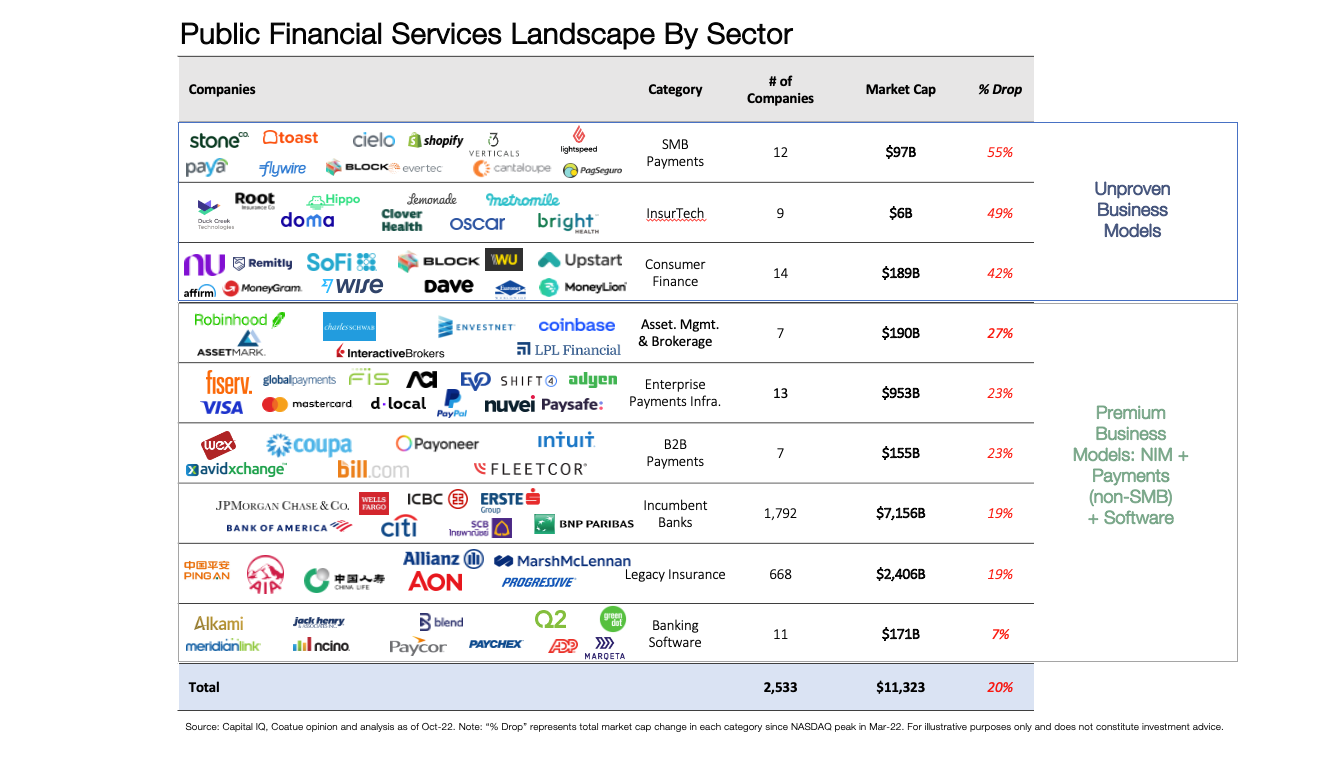

Not all fintech businesses and business models are created equal. Newer and in some cases unproven business models that have been hit harder in the public markets are consumer finance, insurtech and SMB payments, according to the report.

Source: Coatue Whitepaper: Fintech and the Pursuit of the Prize, October 2022.

Source: Coatue Whitepaper: Fintech and the Pursuit of the Prize, October 2022.

Public fintech

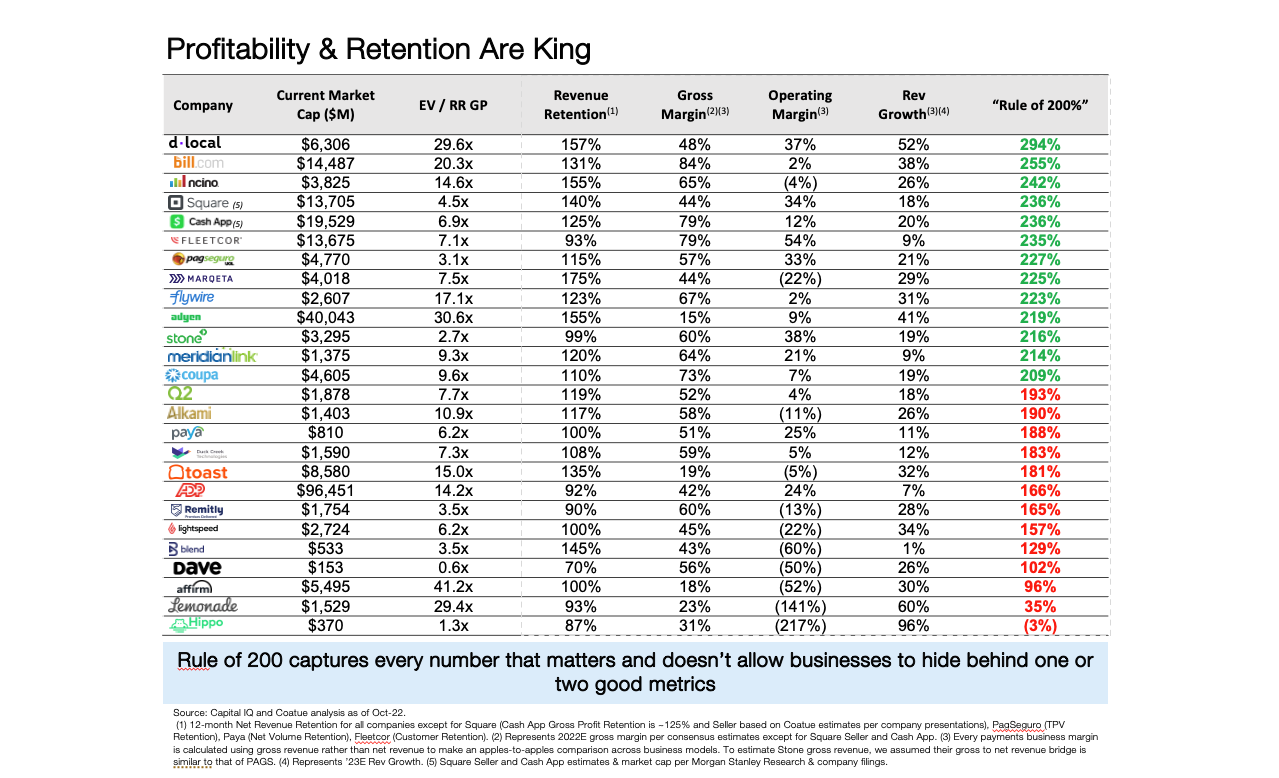

Coatue analyzed the strength of public financial services businesses across four measures: revenue retention, gross margin, operating margin and revenue growth. It then used its “rule of 200%,” which states that if those four factors combined add up to 200% or more, a company is in a stronger position in this market.

By that measure, public fintechs leading on the list are Uruguay-based cross-border payment provider dLocal, Palo Alto, California-based back office financial startup Bill.com and North Carolina-based banking platform nCino.

Source: Coatue Whitepaper: Fintech and the Pursuit of the Prize, October 2022.

Sectors for investment in 2023

“It’s very clear that it’s easier than ever to offer financial services, whether as a standalone business or as part of incremental margin and revenue in an otherwise non-financial business,” said Ben Savage of Clocktower Technology Ventures. “And we believe that trend is going to continue for the rest of our lives.”

With the slump in new tech listings in 2022 and the nosedive in value in public technology stocks including fintechs, where do investors see opportunities in 2023? Here are some sectors that stand out.

B2B fintech

Coatue continues to focus on B2B fintech, Gilroy said. Based on an analysis of the firm’s investments the best business models are in B2B. That’s because business-oriented financial services tend to have lower churn — compared to consumer fintech — and business customers often grow over time, increase spend and provide opportunities to cross-sell with new products.

There is also opportunity in a “verticalized approach, whether you’re going after landlords in the real estate market or restaurants,” Gilroy said.

Emerging markets

Emerging markets present another growth opportunity for fintech startups.

“There’s a lot of underserved communities around the world in terms of access to even the most basic financial products,” said Emily Man, a principal at Redpoint and an investor in the firm’s early-stage practice in fintech and B2B software.

Coatue noted in its report that “for incumbents who often struggle with customer service and innovation, doing business in emerging markets is practically impossible due to the increasing rate at which locals are coming online.”

Latin American fintechs that have gone public include cross-border payments dLocal, neobank Nubank and e-commerce platform MercadoLibre, which went public in 2007.

CFO stack

Then there’s the so-called “CFO stack,” or technologies that would make a finance executive’s job easier.

“There’s a tremendous amount of digitalization yet to come. A lot of that is around payments, but a lot of that is also around what we would characterize as the CFO stack, all of the different functions a CFO might ultimately have to navigate,” said Savage.

Areas of innovation in this stack include tackling expense management, payroll and benefits, stock allocation, business analytics, financial planning and accounting.

“The opportunity areas in fintech focus on the boring areas of infrastructure, fraud, payment operations, compliance, and taxes. CFOs will be more focused than ever on impact to the bottom line,” Victoria Treyger, a general partner at Felicis, said via email. “Fintechs that can demonstrate an improvement in payment authorization rates, better reconciliation rates, or reduction in fraud that is measurable will weather the downturn.”

Owning the balance sheet

Becoming a bank is expensive and time consuming in the U.S., according to Coatue, but can ultimately provide longer-term stability for a fintech company.

With that in mind, many fintechs are applying to get banking licenses in order to hold customer deposits, manage money transfers and offer loans instead of partnering with an established bank. Square received a banking license in March 2021 to be able to originate loans through Square Financial Services. Revolut has a banking license in the European Union but has yet to be approved for a banking license in the U.K. Neobanks Nubank and Chime are not licensed as banks.

“In a rising interest rate environment, legacy banks, insurance providers, and asset managers have the potential to weather down cycles better than capital-light business models, e.g., insurtech and consumer-facing fintech,” said Coatue in its report.

“Through this last cycle, balance sheets have kind of been a bad word within financial services, and we’re learning that owning the balance sheet, whether you’re consumer facing or business facing, puts you in control of your own destiny and takes you away from the need to maybe go and partner with somebody and continuously work on these these balance sheet agreements,” said Gilroy.

Looking forward

Last year, the big themes in financial services were infrastructure building, embedded finance, consumer fintech and a big interest in buy now, pay later platforms.

With an increase in interest rates and the market downturn, consumer fintech and lending companies face choppier waters while those focused on enterprise payments have a greater potential for consistent growth in 2023.

We expect consolidation as funding dries up, and fewer companies can scale up.

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

67.1K Followers