It’s late in an economic cycle. Labor is tight, markets are at or near all-time highs, and investment into startups and their backers is proceeding at its fastest clip yet.

Follow Crunchbase News on Twitter

This past July set a record for the number of “supergiant” VC rounds of $100 million or more. And although investors pulled back a bit in August, this summer has been incredibly active. Q2 2018 set records for global venture deal and dollar volume. But Q3 may top that, considering the huge rounds we’ve seen so far.

But how is the venture capital community managing to invest so much? Are more, bigger rounds resulting in more, bigger funds to back them? Short answer: yes. But a rising financial tide doesn’t necessarily grow everyone’s AUM1 equally.

Letting A Thousand Funds Raise

In response to startups gorging on VC money, VCs have only deepened the trough.

A couple of years before the start of the supergiant round era, in 2014, there was an uptick in the number of venture funds raised per year in the United States.

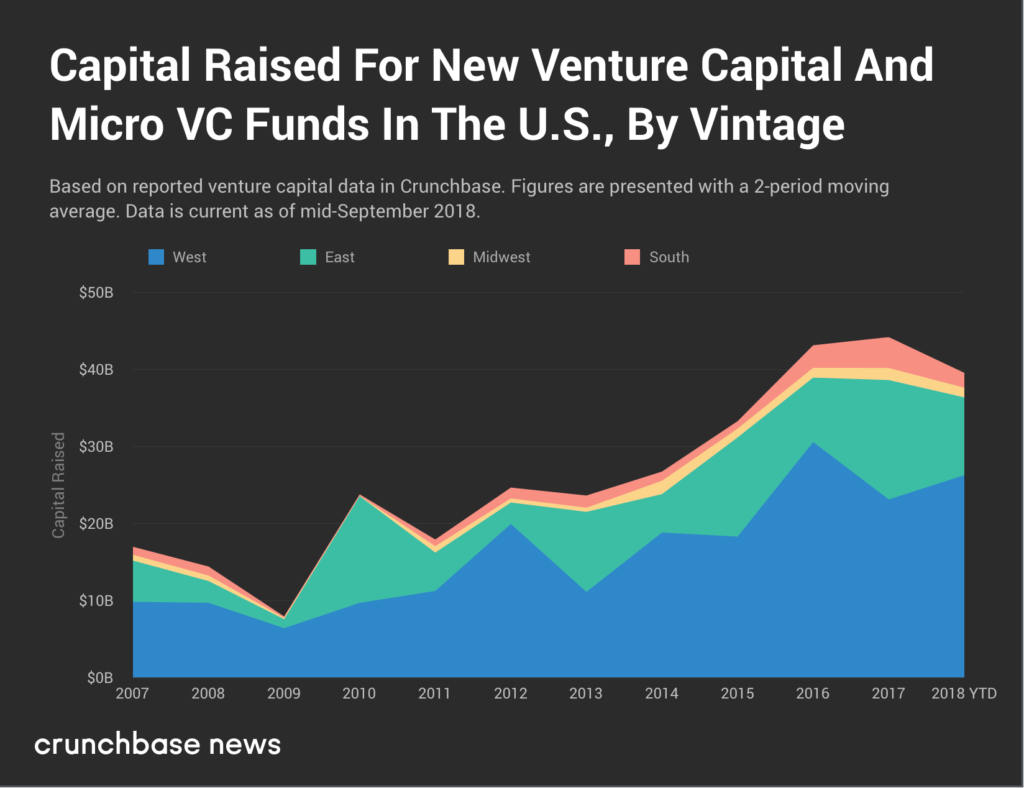

Using Crunchbase data for U.S.-headquartered venture capital and micro VC funds, we plotted the number of new funds raised per year since 2007.

Over the past decade, a lot of new fund managers entered the market as a prior generation of founders and early employees transitioned to the investment side of the business. Data suggests that rate of new fund announcements has slowed recently, but it’s still above historical average.

With a little over a full quarter left in 2018, it’s quite possible that the number of new venture and micro VC funds will exceed 2017’s totals. However, as one would expect, this VC fundraising activity isn’t evenly distributed throughout the country.

Supergiants’ Gravity Bend The Market

As we’ve covered before, there is a fair amount of variance in startup activity between the U.S.’s four primary geographic regions. And although every startup investor is unique and driven by their own incentives, investors approach deal sourcing differently depending on where they’re located.

Let’s see how regional variation affects fund size.

Here we excluded micro VC funds. The “micro” in micro VC can refer to either total assets under management or the size of funds they raise (which, typically, us under $50 million). This being said, the data for micro VC fund sizes echoes regular VC. This being said, the data for micro VC fund sizes echoes regular VC.

For the nation as a whole, average fund size has grown consistency since 2014. From a local minimum of $161 million in 2014 to a year-to-date average of $283 million in September 2018, average fund size had a compound annual growth rate of 16 percent.

And as the chart shows, it’s mostly Western and Eastern investors (particularly along the costs) which:

- Tend to raise bigger funds from the outset, because there are generally more startups and on the coasts

- Are the main drivers of the growing national average for fund sizes.

Notice how Southern and Midwestern venture funds aren’t necessarily raising bigger funds in 2018 relative to a decade ago.

The data suggests the result of all this is that the Midwest and the South remain smaller markets for venture investors looking to secure capital from limited partners.

While it’s tempting to think that Midwestern and Southern investors get short shrift for being smaller fish in smaller ponds, that’s not the case. Prior analysis by Crunchbase News shows that, when it comes to exit multiples, startups from the South and Midwest best their coastal competitors. This could be because these companies tend to raise less money, not in spite of that tendency.

Let’s put this in context. The VC market really is in uncharted territory at the moment.

Q3 may end up setting fresh records for startup fundraising, extending already mind-boggling growth from prior quarters. If that happens, it will be largely because of all these supergiant deals. If the era of supergiant rounds continues, even at a more relaxed pace, investors will have no choice but to raise larger funds if they want a seat at the table with future unicorns, or if they want to rub shoulders with deeply-networked incumbents.

Illustration: Li-Anne Dias

Or, “assets under management.”↩

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Europe Quarterly Graphic - 2024 [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/Quarterly-Cowboy-Europe-470x352.jpg)

![Cloud computing device. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/Cloud_Computing-1-470x352.jpg)

![Illustration of a guy watering plants with a blocked hose - Global [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/quarterly-global-3-300x168.jpg)

67.1K Followers