Buyers offer stock as part of the acquisition proceeds in approximately a third of the transactions. For example, earlier this year, Take-Two Interactive agreed to buy Zynga for $12.7 billion in a mix of cash and stock.

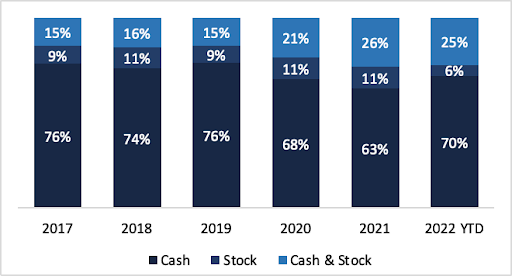

As seen in the chart below where our firm, Allied Advisers, conducted an analysis from various databases of technology M&A deals (7K+deals, over the last five years) where stock was part of the consideration mix. In M&A transactions, stock has been a consideration in ~30% of transactions.

I expect the use of stock to increase given the growth of highly valued private companies who are hiring corporate development teams to focus on M&A. Cash is precious for private companies and they will often offer stock as part of the consideration mix. While cash is generally preferred by sellers due to liquidity, stock consideration could be valuable if structured correctly.

Below are considerations for sellers to evaluate when the proceeds are in stock or a mix of stock and cash. For sellers, it is important to understand the value of the stock and risks associated in accepting stock.

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

Types of shares: Can you get preferred shares; private buyers backed by institutional capital are often hesitant to pay in preferred shares and will instead offer common shares which stand below preferred shares in a liquidation event. For founders, this can be less of an issue given they own common shares in their own company other than the fact they have a higher liquidation preference in the new entity, but the investors in the selling company will be getting common shares vs. preferred shares they held. This brings me to the next point: liquidation preference where the dynamics between common and preferred shares come into play.

Understand liquidation preference: While the top-line valuation number may seem exciting and press worthy, sellers need to understand how share proceeds will be paid upon an exit. Sellers should evaluate if your buyer stock value makes sense considering the overall IPO and M&A market conditions and buyer’s current revenue run rate.

Liquidity options: While cash is superior in this regard, there are private exchanges which may allow you to get liquidity on the stock. Check with the buyer if you can sell shares in these exchanges and if there is a lock-up period etc., which could allow for liquidity. For late-stage companies there is usually a healthy market for trades as investors have strong demand for pre-IPO companies.

Tax considerations: Getting proceeds in stock can create tax issues by getting illiquid proceeds in stock you may not be able to monetize, but the IRS would see this as a gain and come knocking on your door. Sellers should ensure they are getting cash in the transaction which allows sellers the ability to meet potential tax obligations.

Downside protection from stock volatility: The deal document might indicate the purchase price is either a fixed price where one gets a fixed amount at close or fixed dollar amount of shares. In the second case, the seller is prone to fluctuations in value depending on the share price. While we have seen bull markets, the recent tapering in public markets can cause a lot of the deal value to evaporate if not structured correctly. In public companies there is the concept of collars when using stock as acquisition currency. The collar concept can protect the buyer and seller from fluctuations in stock price thereby preserving the value of the deal.

Ask for higher valuation given stock consideration: If there is significant stock in the mix, consider asking for a higher valuation given the risk. Private company stocks have not tapered as much in valuation compared to public companies. It is not uncommon for some of these private companies to still trade at 30x to 50x ARR (and even higher). So, the buyer could pay half the valuation on your ARR and still come out ahead and play this “arbitrage” all day long.

Ask for cash to de-risk: Get some liquidity in cash. Once you have sold your company, you have given up control. Having cash at close monetizes your work and avoids a scenario where if the buyer stock traded below liquidation preference you could get nothing in proceeds. It avoids situations where one could have sold a company in stock to a buyer like WeWork whose stock is less than 10% of its peak value as of April, 2022.

Cap table management creates options: Buyers may not want all shareholders in the sellers’ company in the cap table. This creates an opportunity for angel investors to be cashed out at a premium valuation in cash. Institutional investors are generally okay in accepting stock if they feel they are getting to be part of a bigger story. Institutional investors can also spread their risk profiles across companies allowing them flexibility in considering stock proceeds.

Rollover creates additional upsides: PE backed companies may provide an option to have a “second bite of the apple” which can be larger than the first exit via rollover of proceeds. PE firms run companies carefully with a thoughtful eye on profitable or close to profitable growth which can enhance equity value. In addition, there are tax tools like Qualified Small Business Stock (QSBS) exemption and mechanisms like long-term capital gains tax treatments, which can provide tax savings.

Stock consideration requires additional buyer diligence: On an all-cash deal, due diligence is easier as the seller needs to make sure the buyer has the cash (or access to cash on hand). Where stock is involved, sellers are encouraged to dig deeper into the buyer’s business and understand better their long-term strategy to thoroughly evaluate the stock potential given future consideration is tied to the buyer’s stock enhancement.

While there are many more nuances than this article can cover, an experienced investment banking advisor can help in this regard and create additional options.

Gaurav Bhasin is managing director with Allied Advisers, a global technology-focused boutique advisory firm focused on investment banking for entrepreneurs and investors. The Silicon Valley-based firm, with a presence in Los Angeles, Israel and India, serves entrepreneurs and investors of technology growth companies on strategic advisory including M&A and capital raises.

Illustration: Li-Anne Dias.

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of a guy watering plants with a blocked hose - Global [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/quarterly-global-3-300x168.jpg)

67.1K Followers