In the U.S., there are now plenty more VC funds, and they’re raising more money than ever. That’s great news for most founders, and the folks looking to get into the business of funding them.

Subscribe to the Crunchbase Daily

It’s a trend we covered almost exactly one year ago, and it seemingly continues apace today. Last year’s central contention, that the biggest funds “weigh on their smaller counterparts,” holds especially true now. 2018 proved to be a banner year for venture capital fundraising for VC fund managers across the AUM spectrum, but the biggest funds continue to capture much of the upside as more capital flows into private technology company equity.

This comes at a time of heightened “supergiant” VC deals (of $100 million or more), where a small subset of tech companies are able to raise in single private financing round what most investors hope to raise for a whole fund, often in lieu of raising from public markets. Additionally, private-market deal volume and average transaction size have crept up over the years, at all stages, and combined these factors press more capital into the service of VCs.

A Rising Market Raises All Funds

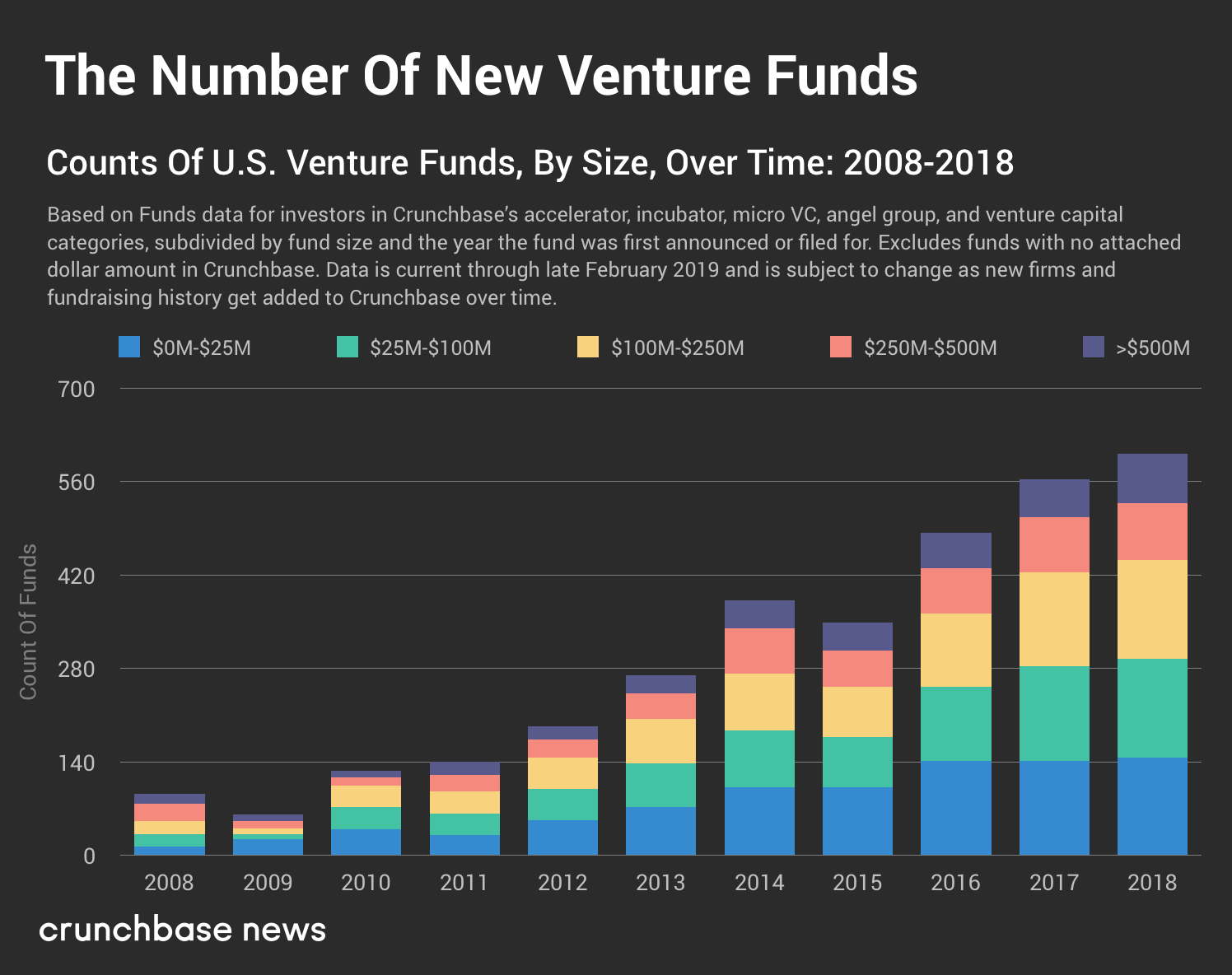

The data we’re using is based on the set of funds raised by U.S.-based investors in Crunchbase’s venture capital, micro VC, incubator, accelerator, or angel group categories (plus those with unassigned categories), which we’ll collectively refer to as “venture funds.” We segmented these funds by the amount of capital raised and fund vintage (e.g. the year in which the fund was announced or first filed for, whichever date is listed for the fund in Crunchbase), and plot our findings in the charts below. These figures are based off of reported venture fund data and may change slightly as new investor profiles and their historical fund-raising activity is added to Crunchbase’s dataset.

The overall number of startup investment funds raised per year extended an upward trend through the end of 2018. Note that these findings differ slightly from our September 2018 analysis of venture fundraising patterns, which indicated that new fund creation may have peaked in 2016. The primary difference here is the mix of investors we’re examining. This analysis also includes incubators, accelerators, angel groups, and funds raised by firms with no assigned investor category.

Although the number of funds announced annually continued to grow over time, the general mix of funds hasn’t all that much. Especially in the past five years or so, sub-$100M venture funds have accounted for between 55 and 61 percent of new funds announced by U.S. firms.

2018 was a banner year for truly huge venture funds. Crunchbase News covered many of those new funds when their SEC filings or public announcements hit the wires. These include $1.85 billion raised by Bessemer Venture Partners for its tenth flagship venture fund, several multi-billion dollar funds from Sequoia Capital, $1.375 billion raised by General Catalyst’s ninth fund, $1.65 billion raised across Index Ventures’s ninth venture fund and second growth fund, and $1.975 billion for two funds raised by Lightspeed Venture Partners. Lightspeed and Index’s funds were announced on two subsequent days in July 2018, around the time supergiant deal volume peaked that year.

Money Flows Uphill

The biggest funds continue to weigh on the venture capital market. The chart below shows just how skewed venture fundraising has become.

According to Crunchbase data, roughly 84 percent of the capital raised by U.S. venture investors went into funds raising $250 million or more. Again, this coincides with a dramatic uptick in supergiant venture capital rounds (at all stages) and a bull market that kicked late-stage venture deal-making into high gear.

But with roughly seven percent of the total capital raised, sub-$100M micro and “nano” VC funds claimed the smallest slice of LP backing since the 2008-2009 financial crisis, after which a slew of small funds sprouted up.

On the fundraising side, the bulk of AUM growth in VC has ultimately redounded to the benefit of the biggest investors already in the game. Although funds in the highest size class, half-a-billion dollars and up in this analysis, account for just twelve percent of the new venture investment vehicles announced in 2018, these giant funds netted about 66 percent of reported capital invested. This sets a new level of top-heaviness in the venture capital GP-LP fundraising market.

In this respect, not much has changed since last year, when we highlighted a number of trends that still appear to be still in play:

- The SoftBank Vision Fund inched closer to its $100 billion target and keeps unloading truckloads of cash (its 2018 deals range between $100 million and $4 billion) onto some of the world’s highest-valued private tech companies.

- The prevalence of supergiant VC rounds of $100 million or more only intensified over the course of 2018 and has continued into 2019. (We’re tracking all the rounds over $250 million here.)

- Average venture fund size around most of the U.S. is growing as bigger VC funds bend the fundraising curve. (Note, this trend wasn’t as pronounced in the Midwest, where average fund size has remained fairly steady since 2014, trailing the national average.)

The number of new venture capital funds announced or filed for continued to rise, year over year, also seemingly unabated. What speeds also slows; what goes up will eventually come down. But at least for now, a lot of emerging managers see an opportunity to enter the venture investing game, even as the big whales at the table re-up the stakes.

Illustration: Li-Anne Dias

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of pandemic pet pampering. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/2021/03/Pets-2-300x168.jpg)

67.1K Followers