Investors are sounding the alarm that the funding environment for startups has changed dramatically compared to last year.

Y Combinator last week warned its portfolio companies to “plan for the worst.”

Pete Flint at NFX recently listed 39 strategies for startups to deal with the downturn. “Only this downturn is different,” he wrote. “It’s bigger. And it’s likely to last much longer.”

Sequoia Capital gathered its founders on Zoom to address this “crucible moment.” In its presentation, the firm said “the cost of capital has fundamentally increased.” It also noted that crossover funds active in funding private companies are significantly impacted and “are tending to wounds in their public portfolios, which have been hit hard.”

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

Venture investing fell in the first quarter of this year for the first time in two years, per Crunchbase data. We expect that downward trajectory to continue for the foreseeable future.

In 2021, by contrast, funding doubled year over year as growth equity investors increased their commitments significantly to invest in private companies, and venture funds raised larger amounts of capital.

Is the pullback here?

In light of these trends, have the most active investors actually pulled back their spending this year?

To get a sense of that, we analyzed the spending patterns of the most active investors—based on their investment pace between Jan. 1 and May 24, 2021—to see how it compares with the same time periods in 2020 and 2022.

In this list are a mix of well-funded venture firms, alongside growth equity investors who piled into private company investing as technology stocks boomed after the initial pullback in the first quarter of 2020.

Active investors maintain deal pace

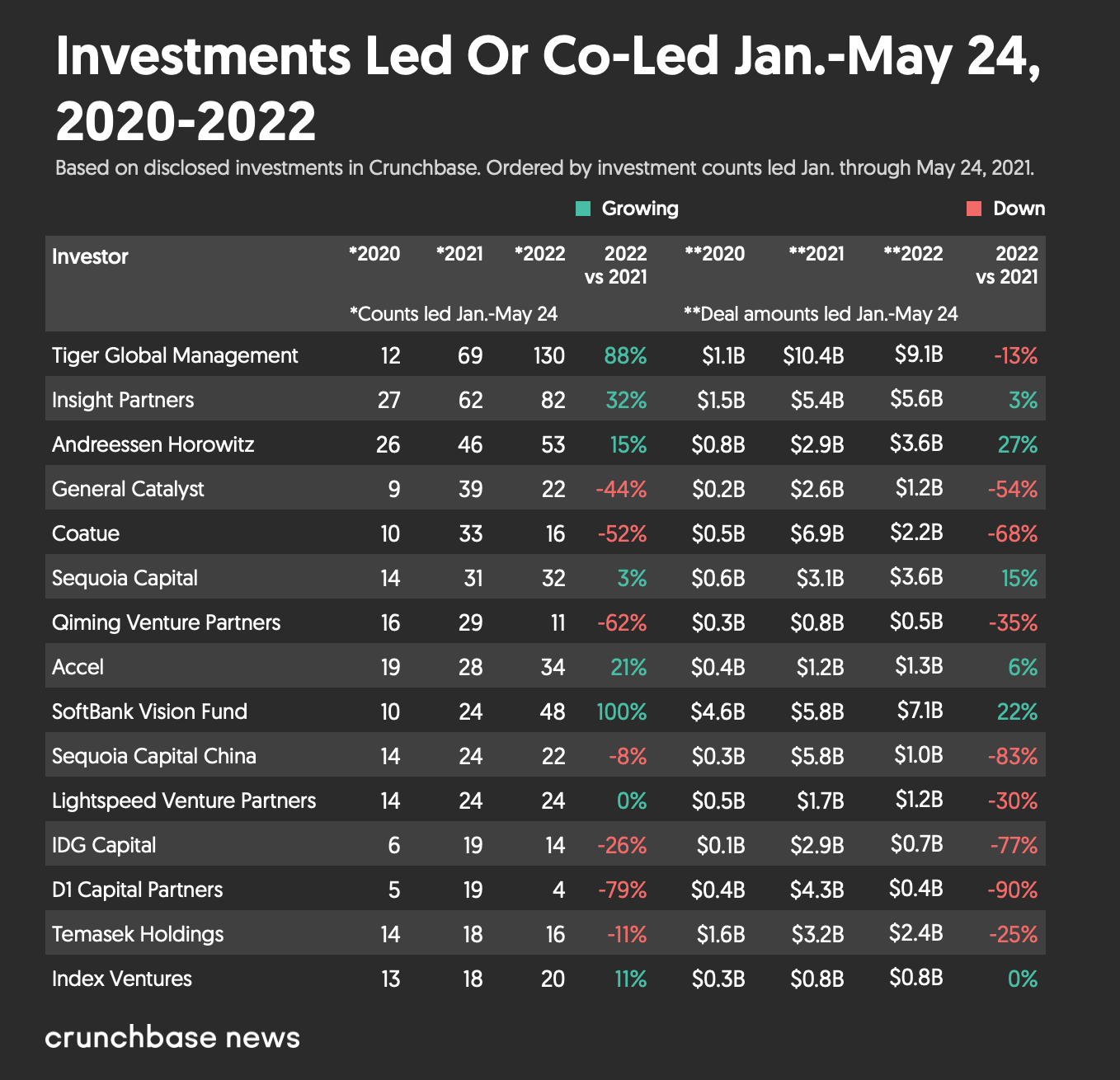

Interestingly, far from pulling back on the number of investments they’re making, the most active startup investors in recent years have done more deals this year than last. SoftBank Vision Fund, Tiger Global and Insight Partners are all up significantly when you count the number of deals they did between Jan. 1 and May 24, 2022, compared to the same time period in 2021.

These funds are still active. That’s despite the Softbank Vision Fund reporting significant losses. Tiger Global has shed major positions in public technology stocks and also recorded notable losses.

The increase in funding pace from these growth equity firms in early 2022 is in part due to deals completed or in process before the write-off in technology stocks, and possibly in part a delayed assessment as to whether this is going to be a sustained downturn.

At the beginning of the pandemic, the market crashed but came back over the following months. Then it skyrocketed as consumers stuck at home adopted digital services.

Deeper into the pandemic, many more companies went public in 2021, compared to prior years.

This moment is perceived differently by traditional venture firms. As opposed to growth equity firms, VCs might consider now to be a time to invest, provided they have the funds at their disposal.

As crossover investors tend to their wounds in the public market, there could be a market opening for venture capitalists to lead startup investing once again, albeit at lower valuations.

We’ve already seen Accel, Andreessen Horowitz and Index Ventures increase their investing pace this year, though not as dramatically as the leading growth investors. Sequoia Capital and Lightspeed both remain on pace with 2021.

Who’s pulling back?

Some firms have already shown dramatic drops in the number of deals they’ve led so far in 2022 compared to last year. D1 Capital Partners, Qiming Ventures, Coatue and General Catalyst are each down by more than 40% for deals led. Contrast this with Jan. 1 through May 24, 2021, where each of these investors led more deals than the prior year for the same timeframe.

Based on public statements by growth equity investors, we expect the reset to continue.

Led or co-led by amounts

When it comes to rounds led or co-led by dollar amounts, most firms are down year over year, with the exception of Andreessen, Softbank Vision Fund and Sequoia. This should not be confused with the actual amount a firm invests, however, as more than one firm can invest or lead a round.

Others are staying the course: Accel, Insight Partners and Index Ventures are all on track this year with 2021 deal amounts they led or co-led.

But a larger proportion of the firms listed show deal sizes have dipped when compared to 2021. Those dips indicate a softening of the venture markets.

Early days

It’s worth keeping in mind that many deals announced in the first quarter of 2022 were actually closed in the fourth quarter last year. That means it might take a little longer for changes based on the new market conditions to percolate through.

Month to month investment counts for an individual investor also tends to fluctuate, so a one month decline is not necessarily indicative of a slowdown.

It’s likely these numbers will continue trending downward, but perhaps not consistently for every active investor.

Many venture investors say that even if the overall market is retreating, they’re still investing. And many growth equity investors have signaled that they will invest earlier or slow down.

Overall, the private funding markets are beginning to adjust to the reality that this is not a blip. That it is, rather, a more sustained revaluing of public technology companies.

The question on everyone’s mind is: When does this end, and what do we reset to?

Methodology

The data contained in this report comes directly from Crunchbase, and is based on reported data. Data reported is as of May 24, 2022.

Note that data lags are most pronounced at the earliest stages of venture activity. We might be missing deals led for individual investors if a funding has not yet been announced.

The most recent /month/quarter/year will increase over time relative to previous quarters.

Please note that all funding values are given in U.S. dollars unless otherwise noted. Crunchbase converts foreign currencies to U.S. dollars at the prevailing spot rate from the date funding rounds are reported. Even if those events were added to Crunchbase long after the event was announced, foreign currency transactions are converted at the historic spot price.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Computer generating AI data. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/AI-generated-470x352.jpg)

![Illustration of agentive AI brain - Global - Quarterly. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/Agentive_AI_global-470x352.jpg)

![Illustration of a guy watering plants with a blocked hose - Global [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/quarterly-global-3-300x168.jpg)

67.1K Followers