Editors Note: This is the first part in a two-part series looking at the lessons learned from the financial crisis and venture capital’s pandemic rally. Read Part 2 here.

Former U.S. President Harry S. Truman famously once said, “There is nothing new in the world except the history you do not know.”

The same holds true for funding cycles. As investors and founders continue to reel from the truly unbelievable circumstances kicked off in 2020 by the global COVID-19 pandemic, one can’t help but harken back to the dramatic impact of the 2008 financial crisis.

The effects of the financial crisis and the pandemic differed dramatically, as we’ve visualized here through the data; the financial crisis put the brakes on funding, while the pandemic was an inflection point.

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

Despite the decrease in funding in the aftermath of the financial crisis, company formation and seed funding kept growing due to underlying technology trends. The emergence of seed led to a completely new wave of innovation.

As the business world moves into another period of turmoil in 2022, let’s take a look at what we can learn from these two recent periods of economic upheaval.

The 2008 financial crisis

Without question, Crunchbase data shows the financial crisis of 2008 had a significant impact on private company financings, with the slowdown starting toward the end of that year.

Sequoia Capital sounded the alarm with its “RIP Good Times” presentation in October 2008, warning its portfolio companies to buckle up and manage costs to increase their runway as the funding markets were no longer intact.

A huge deficit in funding in 2009 ensued. It wasn’t until 2011 that funding picked back up to 2007 levels.

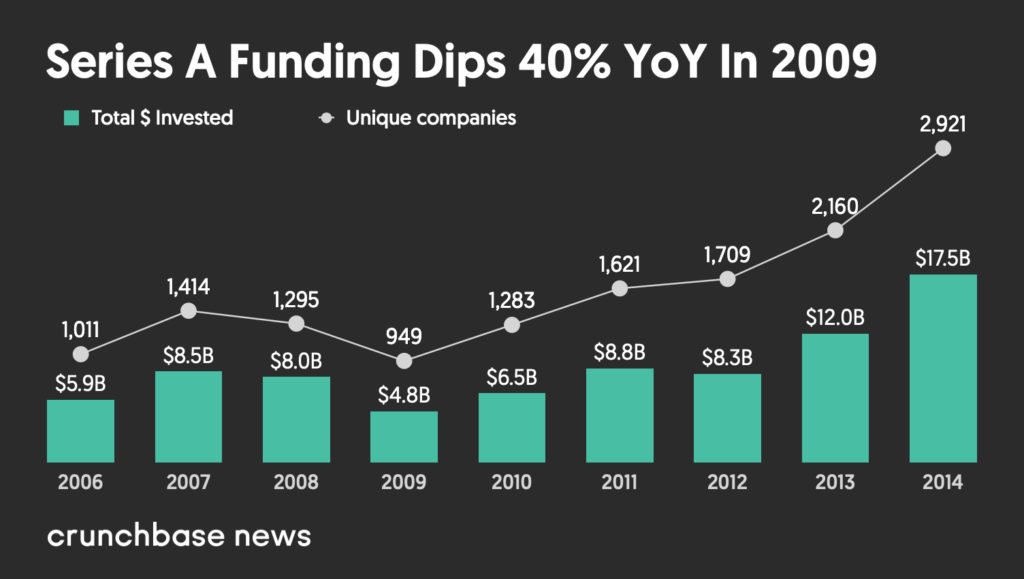

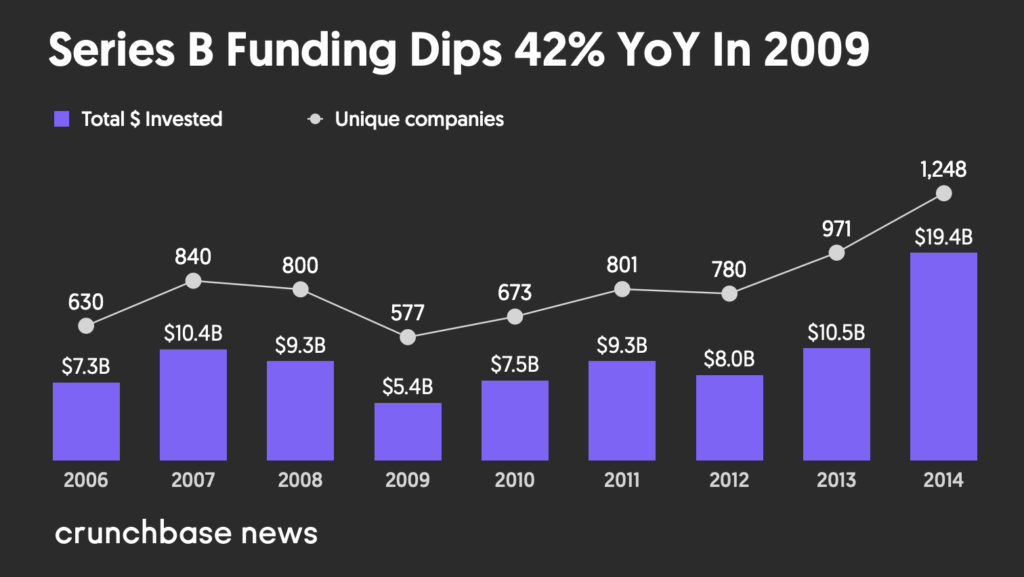

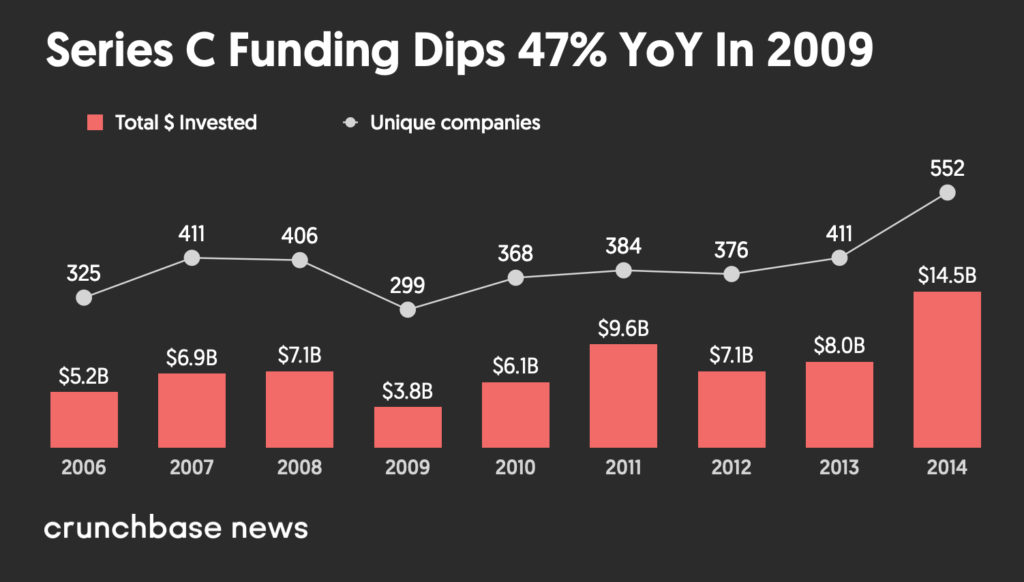

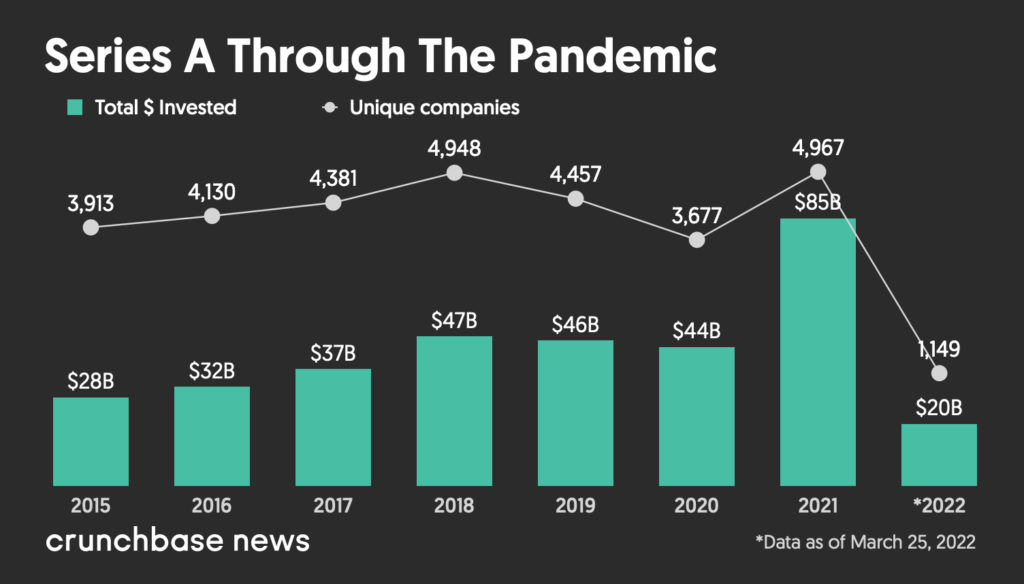

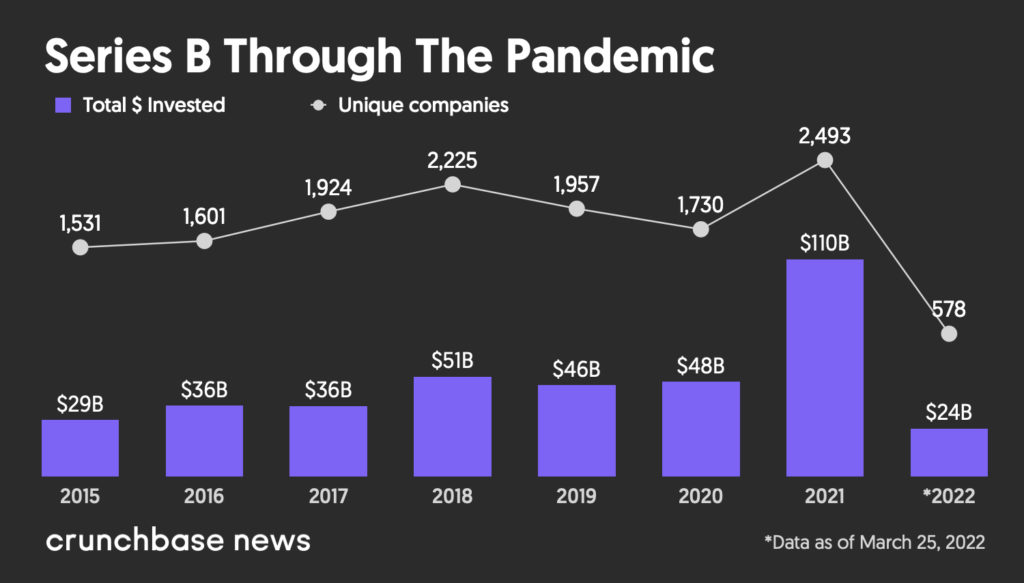

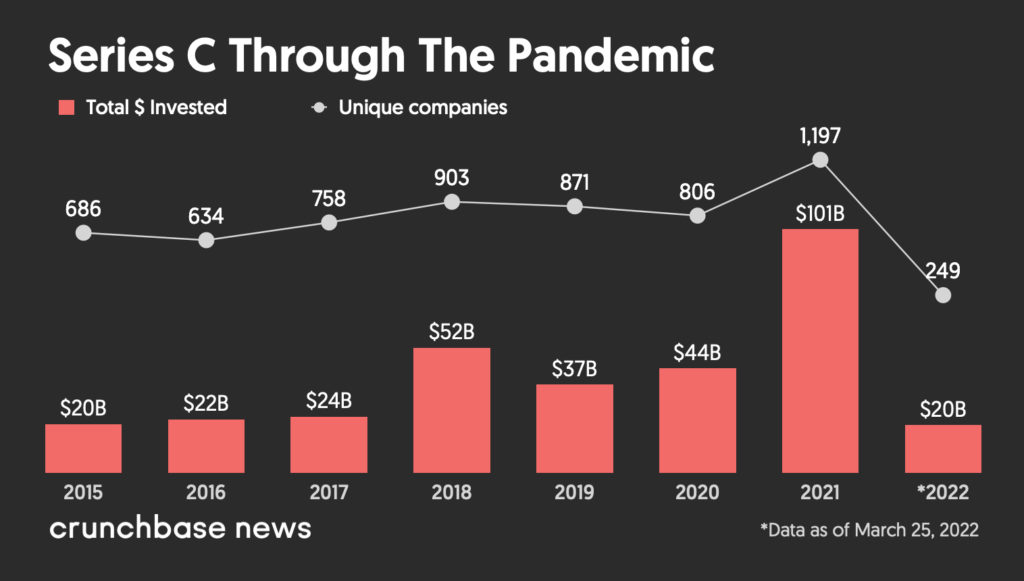

Funding amounts at Series A, B and C dipped between 40 percent and 47 percent in 2009 compared to funding in 2008, according to Crunchbase data.

Unique companies funded from Series A through Series C fundings declined as well in 2009 between 26 percent and 28 percent year over year.

It took a couple of years for 2007 and 2008 funding amounts and counts to be met or exceeded again.

Seed funding sprouts into an institutional class

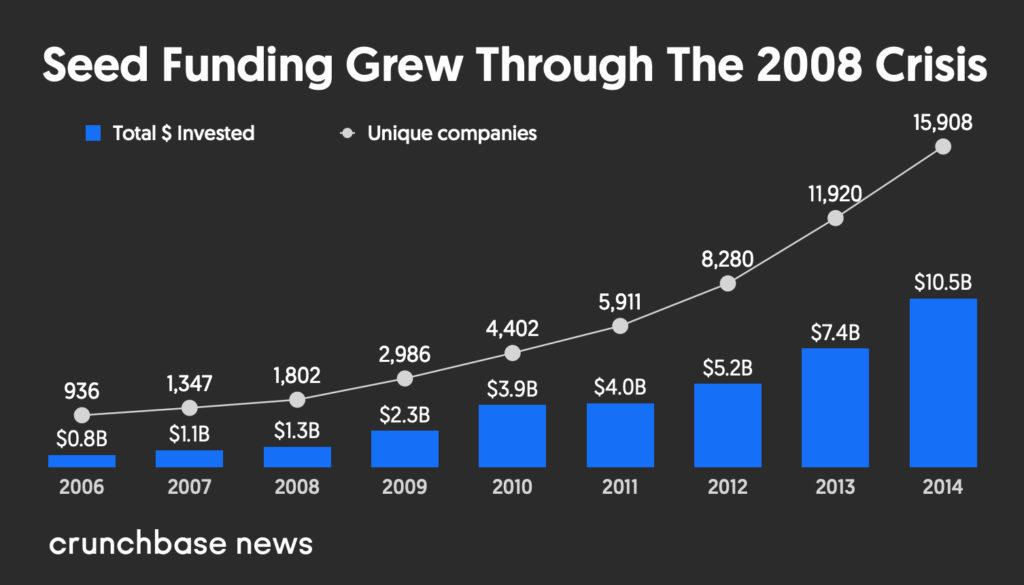

Still, throughout the 2008-2009 dip, a completely new funding stage was in the process of establishing itself alongside the growth of cloud and mobile technologies.

Seed emerged as an institutional asset class during the Great Recession, with investment in the youngest startups no longer left to friends and family or the occasional angel.

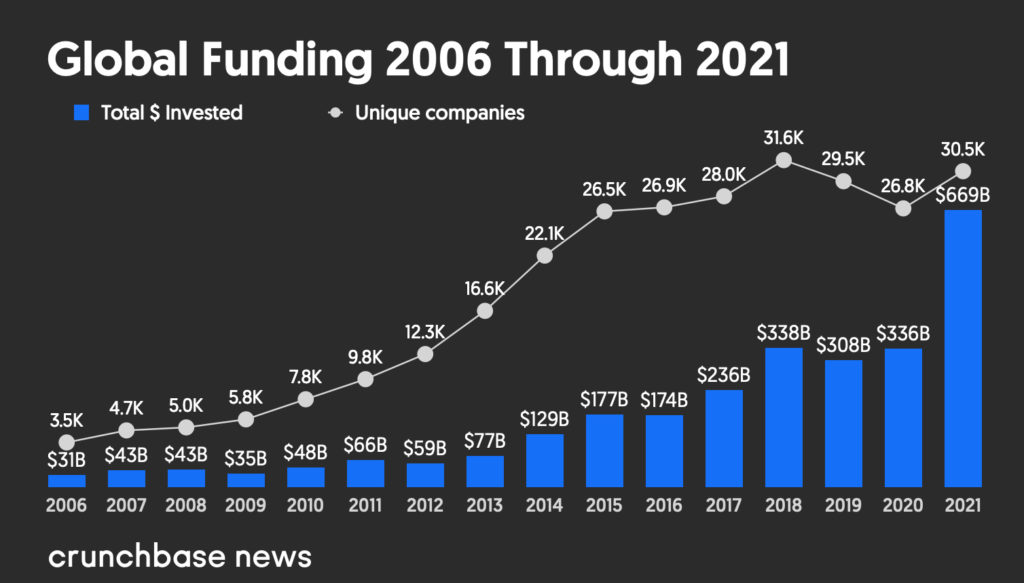

And seed investing showed continued growth post 2008, according to Crunchbase data, reaching close to 16,000 companies which raised funding at that stage in 2014 compared to fewer than 1,000 companies eight years earlier in 2006.

The financial crisis of 2008 slowed funding for early- and late-stage ventures, but not funding at seed and not new company formation. New companies were created and funded throughout that timeframe at a growing rate despite the slowdown in funding post-seed.

This turns out to be the more significant trend of the financial crisis.

What we saw during the pandemic

As we entered the pandemic in the first quarter of 2020, we saw some early signs of a slowdown, per Crunchbase data. Sequoia Capital again issued a warning, this time calling the nascent pandemic a “black swan” event.

But the expected slowdown did not materialize in later quarters in 2020, and funding by and large was within a 5 percent range at Series A and B. And Series C, in fact, went on to grow around 18 percent in 2020 versus 2019.

Then in 2021, funding was off to the races with more than 93 percent at Series A and 132 percent growth at Series C compared with 2020.

What the pandemic highlighted was a trend that had been quietly brewing throughout the last decade.

Rather than a narrative of cycles of fundings with ups and downs, we saw a paradigm shift: a complete overhaul of industry by technological innovation.

Every area of our society—from entertainment to transportation, manufacturing, commerce, health care, energy and finance—are in the process of being transformed. What that means for society and culture is being negotiated at many levels, and the process will not be even. Legacy businesses are being transformed, as are the very investors that fund technology startups.

It turns out the technology trends that led to the rise of seed-stage venture and the force that recreated industries was also the catalyst that led to more than 30,000 venture-backed startups receiving funding in 2021—up from 3,500 companies in 2006.

Last year was by far a record for global venture capital, with $669 billion invested in startups worldwide. That inflection point was built off of more than two decades of innovation.

As we head into the second quarter of 2022 with concerns about potentially overvalued companies, pandemic-era purchasing trends that might be waning, supply chain issues, inflation and a slowdown in the public markets, there is anxiety that we are heading toward another slackening in private financing.

But funds raised by venture and private equity firms in 2022 have not yet slowed down.

And should fundings and valuations fall in 2022, companies should buckle up for some bumps, but the seismic changes wrought by the last decade in venture capital are here to stay.

Methodology

The data contained in this report comes directly from Crunchbase, and is based on reported data. Data reported is as of March 25, 2022.

Note that data lags are most pronounced at the earliest stages of venture activity, with seed funding amounts increasing significantly after the end of a quarter/year.

All funding values are given in U.S. dollars unless otherwise noted. Crunchbase converts foreign currencies to U.S. dollars at the prevailing spot rate from the date funding rounds, acquisitions, IPOs and other financial events are reported. Even if those events were added to Crunchbase long after the event was announced, foreign currency transactions are converted at the historic spot price.

Glossary of funding terms

Seed and angel consists of seed, pre-seed and angel rounds. Crunchbase also includes venture rounds of unknown series, equity crowdfunding and convertible notes at $3 million (USD or as-converted USD equivalent) or less.

Further reading:

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of remote meet on cellphone, unicorn chess piece and money. [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/business-strategy-470x352.jpg)

67.1K Followers