Earlier today, the Securities and Exchange Commission (SEC) dropped a cease-and-desist order concerning an initial coin offering (ICO), detailing precisely why it fell afoul the rules.

The SEC’s action comes at an interesting moment for the broader ICO market. ICOs are a startup fundraising technique that roared to popularity in mid-2017 on the back of the performance of the Ethereum blockchain and its ether token.

Follow Crunchbase News on Twitter & Facebook

According to CoinDesk, the ICO in question, Munchee’s launch of the “MUN” token, has refunded the $15 million it raised.

Since the summer rush of ICO activity — the noise of which induced more than a few venture players into the game — may be slowing. (According to CoinSchedule, a popular ICO-tracking site, dollar-volume of ICO activity has dramatically fallen. However, CoinDesk’s data points another direction.)

Regardless, as even some crypto-focused startups avert from the ICO route, the SEC is stepping up its game. So what’s going on with American ICO regulation? Let’s find out.

The ICO

Munchee is a food-focused app that bills itself as “a visual guide and social-networking app for food.”

Confused that you haven’t heard of it? Don’t be. According to Crunchbase, the company has an opaque funding history, limited coverage, and a small staff. None of that is a sin in and of itself, but that the firm managed to raise so much in an ICO should be illustrative of the heady health of that market.

Heady strength aside, here’s the Munchee splash page:

The firm’s ICO was designed to sell Mun tokens, which had a hard cap, and could be used, for, well, something at some point. Here is how Munchee described it in its white paper:

The Munchee platform will offer a proprietary crypto-token to restaurants and consumers in an effort to incentivize activity on the Munchee mobile app. This will primarily occur when restaurants buy Munchee tokens (MUN) and offer them as a reward to users for their photos, reviews, and social activity related to their experience at the restaurant. The MUN token holds utility for the consumer as a payment method at participating restaurants, for use in the Munchee app for rewards and interactions.

Later in the same document, the Mun token is described as having the “ability to facilitate meaningful advertising and promotion for restaurant owners while building a quality base of content by rewarding content creators for their activity.” Reading as best we can, restaurants would have been able to put up a “bounty” that could be collected, in Mun, by users that take a picture of their food at the location. Here is how the white paper puts it:

This promotion will take place in the form of a listed bounty, with token presented to the end-user as an incentive to post a review of the business and other social activity related to their experience at the restaurant. Upon successful completion of the review, the end-user will receive the bounty.

So you get Mun tokens for reviewing restaurants and the like on Munchee, which can then be used to eat at said food spots.

Perhaps I am a bit slow, but I don’t see hot demand for Mun tokens given the above-described system. Who would buy tokens that, at some later date, may be worth some value at some restaurants, which may or may not be open near the token-holder?

Well, the white paper had some ideas:

Our scheme will implement an in-app Token Membership Plan, which will allow users to move to higher membership level status (Bronze, Silver, Gold, Diamond, and Platinum) by actively participating in the growth of Munchee platform. Munchee users will be incentivized to move to higher membership levels through Munchee’s accelerated reward program.

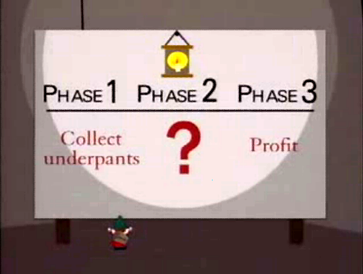

It sounds like users will be rewarded for collecting the tokens and then, to paraphrase South Park, “????,” followed by profit.

What I am trying to point towards here is that it seems that there was little incentive for crypto-investors to buy into the Mun pre-sale unless they were hoping for the tokens to quickly appreciate in value. I doubt that most crypto investors are looking to go long on tokens that my improve their dining experience at some unknown point in the future.

Which is a bit odd, as the white paper includes the following:

This White Paper does not constitute the offering of a security.

Let’s check in on that.

The SEC

In the eyes of the SEC, Munchee was wrong. The regulating entity made it plain in how far Munchee was from being correct.

First, the SEC’s decision:

“[T]he MUN tokens were securities as defined by Section 2(a)(1) of the Securities Act because they were investment contracts.”

This is bad, as you can’t sell a security as a US corporation without running afoul of the SEC if you don’t organize it as a security sale. And, as the white paper had told us, Munchee thought that it wasn’t.

Moving on, here’s part of the SEC’s case as to why it was a security:

MUN token purchasers had a reasonable expectation of profits from their investment in the Munchee enterprise. The proceeds of the MUN token offering were intended to be used by Munchee to build an “ecosystem” that would create demand for MUN tokens and make MUN tokens more valuable.

The SEC goes on to say that potential “[i]nvestors’ profits were to be derived from the significant entrepreneurial and

managerial efforts of others,” and that “[i]nvestors’ expectations were primed by Munchee’s marketing of the MUN token

offering.” The combined meaning of that seems clear: by buying the Mun tokens, the proceeds of which Munchee was to control, the individuals were expecting to accrete value on the work of others. (You know, like an investment.)

And, the SEC went on to refute the obvious complaint:

Even if MUN tokens had a practical use at the time of the offering, it would not preclude the token from being a security. Determining whether a transaction involves a security does not turn on labelling [sic] – such as characterizing an ICO as involving a “utility token” – but instead requires an assessment of “the economic realities underlying a transaction.”

So much for the argument that perhaps other ICOs with similar tokens could skate by the SEC.

The SEC goes on to declare that “Munchee offered and sold securities to the general public, including potential investors in the United States” despite not registering to do so. That means the firm “violated Section 5(a) of the Securities Act.”

You don’t want to do that.

All this is to say that if you are going to pull off an ICO, you are going to want to double check the paperwork. Don’t accidentally sell securities and get into a lot of trouble.

Jesus.

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of a guy watering plants with a blocked hose - Global [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/quarterly-global-3-300x168.jpg)

{kind=link}

67.1K Followers