In the plant realm, we usually envision a seed as something small. In reality, however, dimensions vary immensely—from orchid seeds the size of a dust particle to coconut palm seeds that can weigh over 50 pounds.

The same thing can be said of seed-stage startup investment. While we might think of a typical investment as a couple million dollars, round sizes classified as seed range from tens of thousands to hundreds of millions.

That said, the rise of really big seed rounds is mostly a recent phenomenon. Numbers have grown particularly sharply in the past couple years, coinciding with a sharp increase in overall venture investment.

Search less. Close more.

Grow your revenue with all-in-one prospecting solutions powered by the leader in private-company data.

“The major driver has been more and more capital coming to seed stage,” said Eugene Zhang, founding partner at TSVC, a Silicon Valley-based firm that’s been making seed investments for the past 11 years. Over that time, valuations have grown several-fold, meaning it simply costs more for a significant stake in a promising startup.

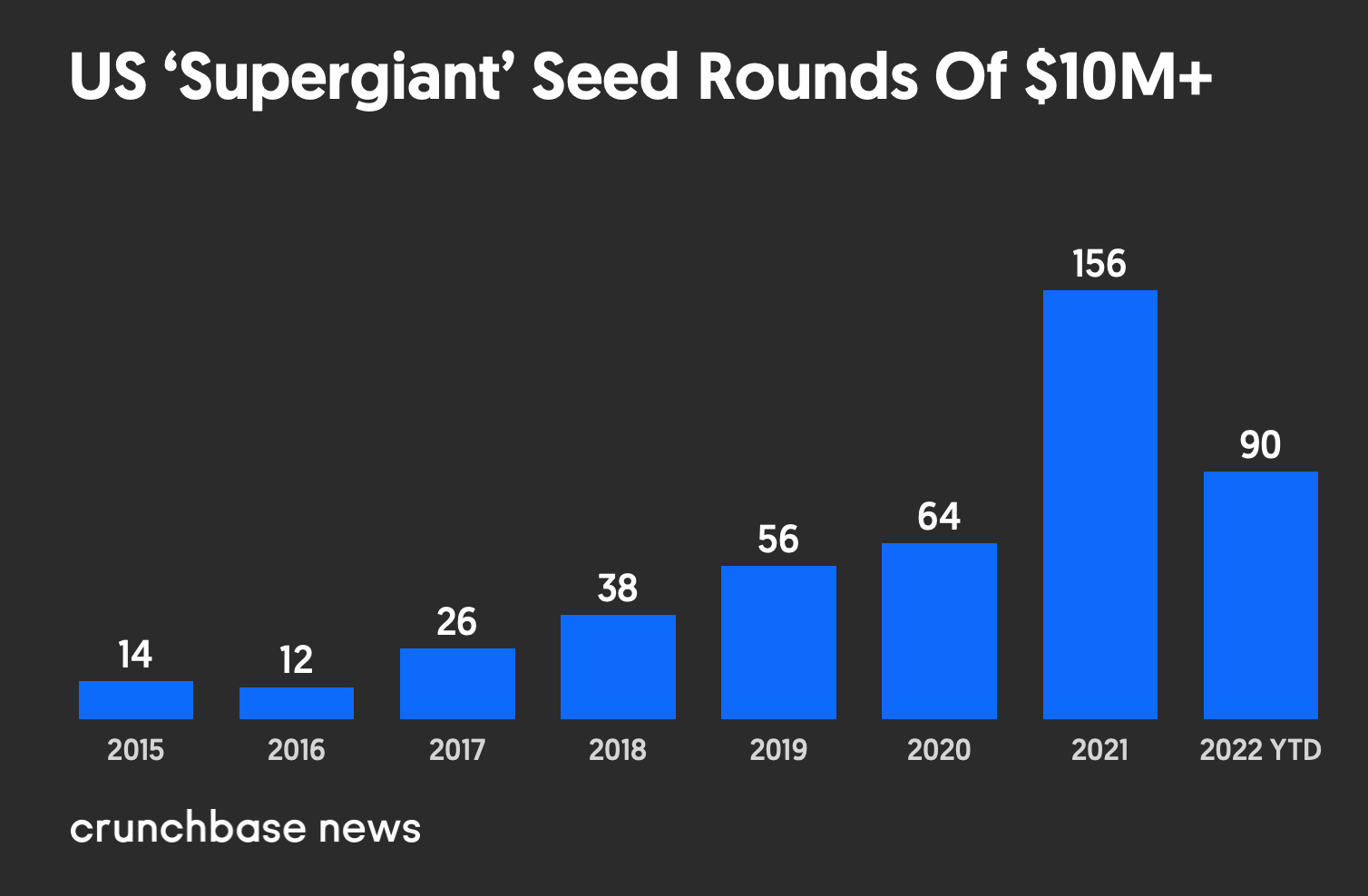

Using Crunchbase data, we analyzed the rise of so-called supergiant seed rounds—investments of $10 million and up—over the past eight years.

These rounds are clearly on the rise in the U.S., with 2022 trending higher even amid a pullback in overall venture investment:

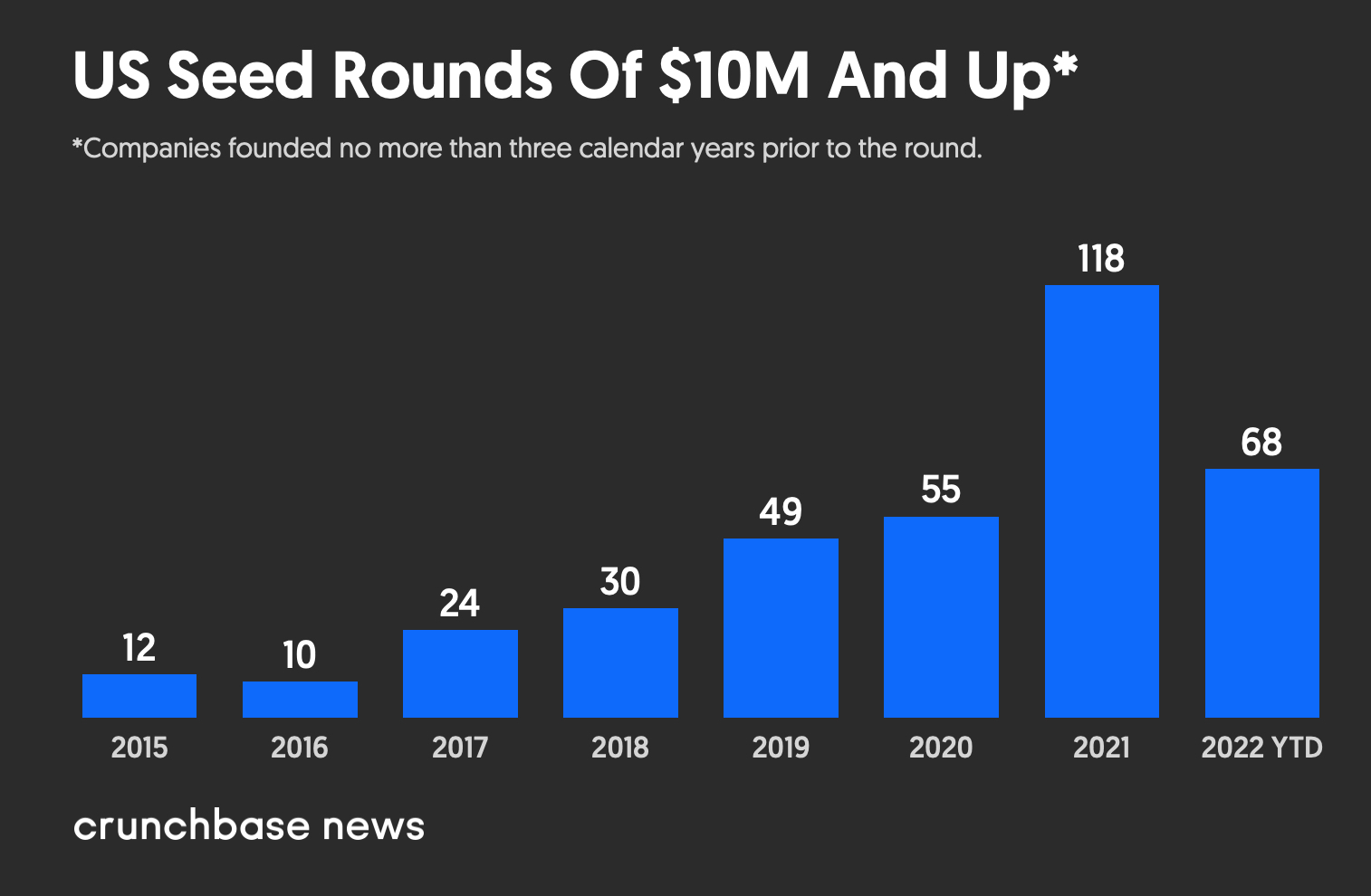

Sometimes bootstrapped companies raise big rounds classified as seed, even though they’ve been around for a while.

To correct for this, we did another chart looking solely at seed rounds for companies founded no more than three calendar years prior to the deal closing. The numbers are somewhat lower, but the trend lines remain pretty much the same:

The companies raising these supergiant seed rounds are a varied bunch, representing a broad range of industries and geographies.

Where the big seeds have gone

The largest seed deal this year went to Yuga Labs, the NFT platform known for its Bored Ape Yacht Club collection. The Miami-based company raised a stunning $450 million round in March, less than two years after its founding.

Among the other biggest rounds, we see a broad sector mix, including fintech, employee benefits, pet care, crypto, spacetech, mental health, drug discovery and many more.

Some seed-round inflation likely stems from stepped-up activity at this stage from deep-pocketed startup investors known for backing big deals. Tiger Global, for instance, which ranks as the apparent spendiest lead startup investor this year, has done 18 seed deals globally in 2022, per Crunchbase data. Andreessen Horowitz has done about a dozen this year.

Pretty much across the seed investor universe, checks are getting bigger. When TSVC was starting out roughly a decade ago, the size of a typical first check was between $500,000 and $1 million, at a valuation of under $5 million.

Now, TSVC Managing Partner Spencer Greene said, the usual first check is $2 million to $5 million, at a valuation of $6 million to $29 million.

A fine line

As seed round sizes approach levels associated with Series A, the two stages can blur a bit.

There are some distinctions, however. Typically, a seed deal is done as a convertible note and a Series A as a priced round, Greene notes, although there can be exceptions. At Series A, it’s also common to expect a company to have a “repeatable go-to-market formula,” which isn’t the case for seed.

Given that seed is the stage at which they can reap the highest multiple return on a successful investment, it’s not surprising to see more multistage investors looking to get in at the earliest point.

Moreover, with cloud-storage, low-code development tools, and a panoply of apps and SaaS tools for managing and scaling operations, one could make a case that startups are able to get off the ground much faster than in the past.

But with higher potential returns comes higher risk. Historically, most seed-funded companies fail, and investors make their profits from the few that prevail. While making bigger bets at the most nascent stages of a company’s formation doesn’t necessarily improve those odds, it does leave a larger sum to lose.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

67.1K Followers