This has been by far the best year yet for Y Combinator, the prestigious Silicon Valley startup accelerator, with two of its biggest portfolio companies debuting on the public markets and the largest acquisition ever of one of its alumni.

Subscribe to the Crunchbase Daily

This year also marks the beginning of a new era for YC, as the program is commonly known, that could see twice as many of its alumni on the public markets by the end of 2021.

Airbnb’s $47 billion debut on the Nasdaq last week in particular is a high-water mark for YC, with a portfolio company that became one of the world’s most recognized internet brands going public.

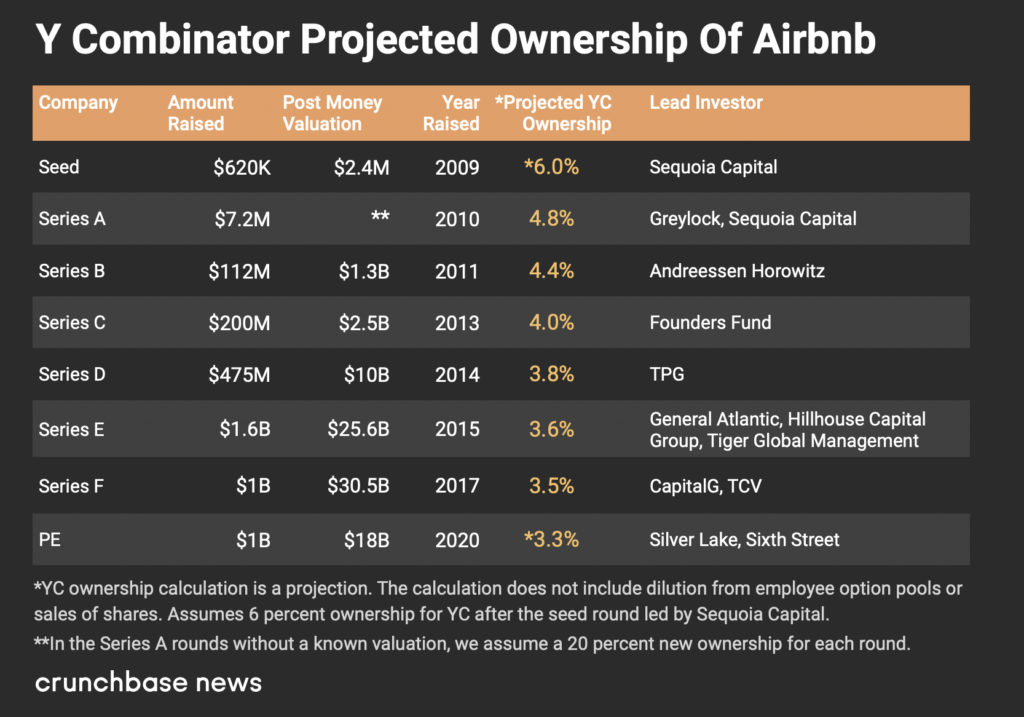

Y Combinator first invested in Airbnb more than a decade ago as part of its winter 2009 class, a cohort of fewer than 20 companies. Then, it provided $20,000 in exchange for a 6 percent stake in Airbnb in the aftermath of the 2008 financial crisis. Airbnb’s last private valuation was $18 billion in April 2020, down from its 2017 valuation of $30 billion due to the pandemic curtailing travel, but the startup rebounded and went on to close its first day of trading with a market capitalization of $100 billion.

Just 24 hours before Airbnb went public, another Y Combinator company, DoorDash, debuted on the New York Stock Exchange at a $39 billion valuation—marking the first-ever exit of more than $10 billion for a YC company. Y Combinator invested in DoorDash more than seven years ago as one of 52 companies in its summer 2013 class. DoorDash’s last private valuation was $16 billion as of June 2020.

Heavy hitters

Both of the public-market debuts have since soared: Shares of Airbnb were up more than 100 percent and DoorDash more than 70 percent from their IPO prices as of Friday. The two leading consumer brands also far surpass previous billion-dollar IPOs for YC companies Dropbox and PagerDuty.

Acquisition record

This year has also been notable for YC on the M&A front, with the largest acquisition ever of one of its portfolio companies in October. That’s when Segment, a customer data infrastructure provider and a startup from YC’s summer 2011 cohort, was acquired by Twilio for $3.2 billion.

The deal tops two previous record-setting $1 billion YC portfolio company acquisitions: The purchase of self-driving technology company Cruise (winter 2014) by General Motors in 2016, and that of gaming streaming service Twitch (winter 2007) by Amazon in 2014.

YC ownership percentage

How much Y Combinator makes from these exits is anyone’s guess, but Crunchbase News has undertaken some calculations we think provide insight into YC ownership percentages over time. We also spoke with Y Combinator President Geoff Ralston, though he neither confirmed nor denied our calculations.

We know from the S-1 registration statements that Y Combinator owns less than 5 percent in each of those four portfolio companies that have gone public.

We also went through the exercise of charting YC ownership of both Airbnb and DoorDash through subsequent rounds. For Doordash and Airbnb, a 1 percent ownership stake nets around $400 million or greater. We believe the amount YC actually nets will be less, as this calculation does not include dilution for employee option pools, and makes certain assumptions about ownership percentages through the rounds.1

What is interesting from these calculations is that dilution is more dramatic in the earlier rounds—as new ownership percentages lessen in the later rounds—and YC gives up less equity.

The YC deal

Entrepreneurs participate in YC “to join our network, our community, because of the advice we give, because we improve their probability of success,” Ralston said. “And so the quid pro quo isn’t like a normal venture capitalist, which is there’s a market for your company and you’re valued at this, and we’ll give you that. That’s not why you do YC.”

Y Combinator has invested in more than 2,500 companies since 2005 when the program launched with the initial eight companies each raising $11,000 with an added $3,000 per founder.

“In 2005 the first batch was eight. In 2011 our batches were 30, 40, 50, 60 (then) went up to 80, and it kind of blew our minds. We had to rethink how we were structured. And now our batch size is trending from 250 to 300 companies per batch,” Ralston said.

In 2011, Yuri Milner and SV Angel2 offered to invest a further $120,000 into each company. Over time, other investors joined Start Fund. This program ended in 2014.

In 2014, Sam Altman, YC’s president at the time, announced the accelerator’s new deal: $120,000 per startup in exchange for a 7 percent stake.

That amount increased in 2019 to $150,000, along with new terms: A 7 percent post-money stake to ensure YC’s stake is not diluted by subsequent unpriced seed rounds a company raises. At the priced seed or Series A, Y Combinator would be diluted both by the new investors, as well as options pools created for employees.

YC recently announced that in 2021 the amount it plans to invest will go down to $125,000 for the same 7 percent allowing them to fund 3,000 more companies.

Y Combinator has changed over the years in other ways as well. “We work with companies way more extensively than we used to,” Ralston said. “In 2011, we launched Startup School. We worked with 10,000 founders at a time. We launched a Series A program, which works with founders 18 to 36 months after the batch, and we’ve launched our growth program and our growth funds.”

The fund has also expanded internationally. Since the pandemic hit, “it is way easier for a company in Southeast Asia, for a company in India, to do YC now,” he said. Previously, YC would fly a company to Mountain View for a 10-minute interview.

“It’s actually super convenient for them to stay where their businesses are during YC and still get the advice,” Ralston said. “There’s no question that remote has been good for our ability to work with founders who are in place and running their businesses in place. I think you’ll see that as a secular change for YC.”

YC’s initial investments by year

To understand how much Y Combinator invests at the pre-seed stage, we charted initial investments in the summer and winter cohort by year. (This chart does not include investments the firm might have made to maintain its ownership at the first priced round, or the increased investment with LPs in 2011.)

M&A

There have been 301 acquisitions of Y Combinator companies, according to our analysis of Crunchbase data. Of these, 47 companies (16 percent) have disclosed their exit prices. It’s worth keeping in mind that there is a large count of missing exit prices and, among this 16 percent, the larger exits are the most likely to have price tags disclosed.

According to our analysis, 2020 has led YC M&A exits, with $4.2 billion in disclosed deals. The number of exits we recorded above $100 million totals 17 companies overall to date, with two at $1 billion or above.

Projected ownership

We calculated ownership since 2012, when exits started coming in for YC portfolio companies, assuming a 2, 3 or 4 percent ownership stake for M&A with disclosed amounts. The returns are compelling when looking at the amounts invested by YC, but the sums per annum were below $100 million until just this year.

When factoring in IPOs, the returns are substantial, though this depends again on ownership percentages. Still, even with an ownership stake of just 1 or 2 percent at an IPO price for DoorDash of $39 billion and Airbnb of $47 billion, YC’s returns mounted quickly in 2020.

2021 and beyond

Y Combinator has 29 more portfolio companies valued at or over $1 billion, per the Crunchbase unicorn board, with a further 11 emerging unicorns.

“I think we’ll probably be on track to double the number of YC public companies by the end of 2021 and not stop,” Ralston said. “Because like I said, the YC companies in the portfolio are coming into their fullness.”

Illustration: Dom Guzman

The amount Y Combinator owns prior to the IPO for DoorDash and Airbnb will most certainly be less than as calculated. It assumes that the YC starting percentage before the first priced round is not diluted by any subsequent unpriced seed rounds. The calculation does not take into account dilution through creating employee option pools or any other preferential terms. It assumes that YC does not offload some shares in high-valued late-stage rounds.↩

SV Angel is an investor in Crunchbase. It has no say in our editorial process. For more, head here.↩

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

![Illustration of stopwatch - AI [Dom Guzman]](https://news.crunchbase.com/wp-content/uploads/Halftime-AI-1-470x352.jpg)

67.1K Followers