Julie Eskay Eagle started thinking in 2019 about how to help small pharmacies branch into a field that for many pharmacists felt both like an obvious offering and also just out of reach: testing and diagnostics, services that often come with complex scheduling and reporting requirements.

Subscribe to the Crunchbase Daily

By the time she and her co-founder got DragonflyPHD off the ground in early 2020, COVID-19 had arrived and the platform was just in time: Organizations from cities and counties to small clinics and nursing homes as well as pharmacists, were trying to join the effort to test, and later vaccinate, their community at a large scale for the potentially deadly virus.

DragonflyPHD, a cloud-based patient management system service, marketed itself as an easy solution for small clinics and pharmacies trying to stay on top of appointment-making, information-tracking and government reporting rules with an interface patients can grasp quickly. Less than two years later, the company had helped their customers schedule and track a million visits with patients.

Many life science startups pivoted their missions and offerings or added services tailored to a world where people stayed indoors and health care systems crumbled under the weight of a brand-new communicable disease. Some companies, like DragonflyPHD, may not have started out trying to focus on the pandemic, but saw huge growth due to the health crisis.

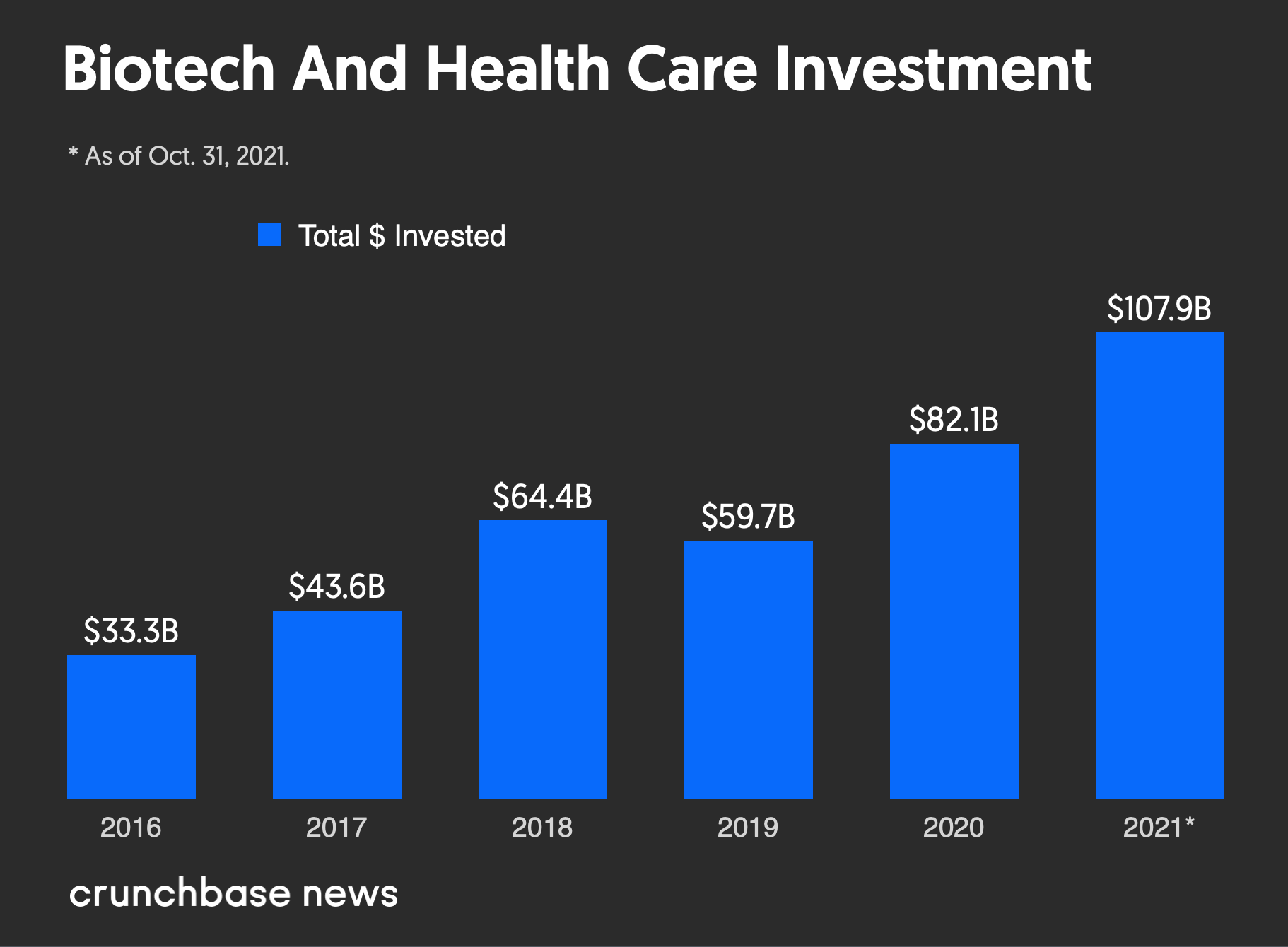

Investments into venture-backed startups in biotech and health care jumped from nearly $60 billion in 2019 to more than $82 billion in 2020, Crunchbase data shows. However, last year’s total investment is already overshadowed by the almost $108 billion poured into startups as of Oct. 31, 2021.

Today, many of those startups and their investors are increasingly thinking about their future in a post-pandemic world while some wonder if a proverbial COVID bubble could be on the verge of popping—and how to avoid being in its path of destruction.

Some startups “made great business decisions to shift focus to COVID and the world needed them and a lot of them did an incredible job,” said Christina Farr, a principal at OMERS Ventures1 who focuses on health tech. “But there’s going to be the question: What’s next when we don’t need quite so many COVID tests? Assuming that that happens, how will they define themselves?”

Early adopters

The pandemic was on investors’ minds early. Peter Parker, co-founder and managing general partner of Mission BioCapital, was on the road in early March 2020 to begin fundraising for the venture capital firm’s fifth life sciences fund, making stops in San Francisco, Los Angeles and New York.

“Every investor who we talked to [in early March] said, ‘Well, I’m hearing about this virus. What do you guys know? How’s this going to affect the life sciences world?’” Parker remembers.

By March 13, 2020, the virus was a pandemic globally and a national emergency in the United States. Parker went back home and struggled through a fundraising slump in April and May, months stymied by uncertainty.

Mission BioCapital’s newly announced $275 million life sciences fund—which is double the size of its previous life sciences fund—was raised mostly via Zoom, Parker said.

“Interest in biotech investing—the interest in limited partners becoming part of early seeds and early-stage funds like ours—came right back,” he said. “And the reason was that pretty quickly, I think people felt that life sciences has some answers, right? If there’s going to be solutions, it’s going to be from this industry.”

Indeed, some answers have emerged. When the pandemic will formally end is anyone’s guess, but vaccines for those 12 and older have helped to slow hospitalizations. Workers are returning to offices that have been mostly empty for nearly two years. Concerts and weddings are back on the calendar, and new therapeutics for the symptoms that come with COVID-19 may be on the horizon.

And with that, startups buoyed by COVID and the firms that have invested in them are trying to stay ahead of the curve again.

Eye on the future

Eskay Eagle expects some customers may scale down when COVID testing needs decline, but the initial technology adoption by pharmacists has also opened the door for them to continue offering certain services, like vaccinations and diagnostics, that many wanted to offer pre-pandemic, but hadn’t figured out how to manage until now.

DragonflyPHD is also launching a program to help companies comply with Biden administration rules that businesses with more than 100 employees keep track of testing or vaccinations among their workers, she said.

“I try to make sure that I don’t have a false sense of security,” Eskay Eagle said. “I think [COVID] has given us a lifeline because we’ve had revenue early in a company’s lifespan, so that’s unusual. But that just sprouted as a result of people being desperately in need of a platform that allowed them to scale this kind of service.”

The industry, Farr predicts, may also find that some things are here to stay, like telehealth options or at-home testing for a variety of ailments. “People just got more comfortable with it, regulators got more comfortable with it,” she said.

But other businesses, specifically those that banked on huge revenue spikes because of COVID testing demand, may have a small window now to start thinking of other business avenues to drum up revenue or investments.

“Every investment we make, we’re asking ourselves a set of questions, and there’s a new set of questions that have been added,” Parker said. “That is: What has changed in the past year and a half that makes us worry about the future of this new investment?”

Unfazed founders

While there was plenty of opportunity for growth for life science startups during the pandemic, some opted to stay out of the game specifically because of a potential COVID bubble.

Naveen Jain, founder and CEO of Viome Life Sciences, said he could see the diagnostics potential his life sciences company had when it came to detecting COVID-19. But he decided to pass on the pandemic pivot because he didn’t want to be derailed by a part of the industry that will, ideally, not be so necessary one day.

“Even though it could have generated hundreds of millions of revenue for us, we made a very conscious decision that it was not going to move us toward our mission,” he said.

Viome last week announced it raised $54 million in convertible funding to research aggressive cancers and chronic diseases and one day come up with new diagnostics and therapeutics for those ailments. That, Jain said, is the company’s primary mission.

Still, the pandemic did help boost sales of Viome’s kits, which allow customers to provide samples of blood or stool to the company and get back a list of recommendations to be healthier as more people started trying to manage their own health from home. And that is a change that Jain predicts will benefit everyone.

“I believe COVID accelerated health care by a decade, that telehealth would not be around for 10 years, but for COVID,” he said. “And I really believe the future of health is going to be delivered at home, not in the hospital.”

Methodology

Startups included in the investment data for this article are venture-funded companies in health care and biotechnology, which includes life sciences.

Illustration: Dom Guzman

Stay up to date with recent funding rounds, acquisitions, and more with the Crunchbase Daily.

67.1K Followers